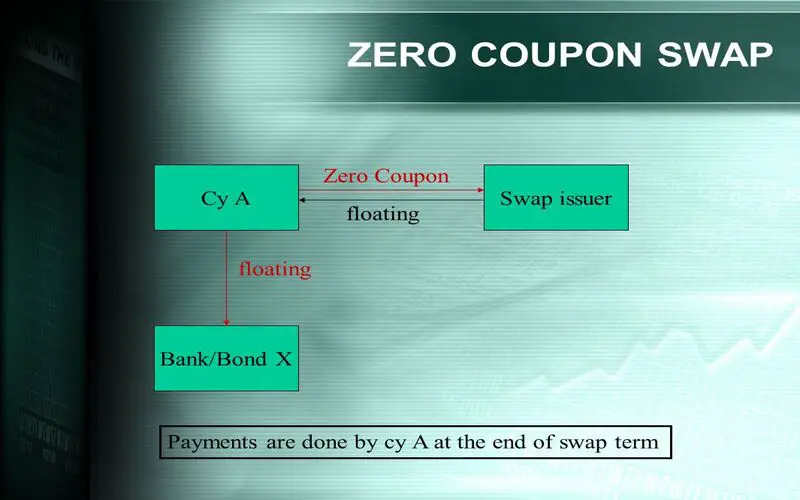

A Zero-Coupon Swap: What Is It?

In a zero-coupon swap, the stream of fixed-rate payments is made as a single lump-sum payment at the time of swap maturity rather than sporadically throughout the trade. The stream of floating interest-rate payments is made periodically, just like in a standard exchange.

Comprehending a Zero-Coupon Exchange

A derivative contract that two parties enter into is called a zero-coupon swap. One party makes floating payments, which vary based on when the interest rate index (such as EURIBOR, LIBOR, etc.) that serves as the benchmark for the rate is published in the future. According to a predetermined interest rate that was agreed upon, each party pays the other.

A zero-coupon bond, which pays no interest during its entire life but is anticipated to make a single payment at maturity, is linked to a fixed interest rate. In actuality, the zero-coupon rate of the swap determines how much of the fixed-rate payment is made. In a zero-coupon exchange, the party on the floating leg must make periodic payments throughout the swap’s contractual life. In contrast, the bondholder on the fixed portion is only required to make one payment at maturity. On the other hand, zero-coupon swaps can be set up to pay out in full for both fixed-rate and floating-rate costs.

The floating party bears a significant default risk due to the mismatch in payment frequency. Compared to a plain vanilla swap, where fixed and floating interest rate payments are agreed to be made on specific dates over time, the counterparty that only receives compensation once the agreement’s conclusion faces a higher credit risk.

Assessing a Zero-Coupon Exchange

A spot rate, also known as a zero-coupon rate, calculates the present value of the cash flows in a zero-coupon swap. The spot rate is an interest rate that applies to a discount bond that pays no coupon and produces just one cash flow at the maturity date. The present value of each fixed and floating leg will be determined separately and summed together.

Since the fixed-rate payments are known ahead of time, calculating the present value of this leg is straightforward. The implied forward rate must be calculated first to derive the current cash flow value from the floating rate leg. Spot rates usually imply forward rates. The spot rates are derived from a spot curve built from bootstrapping, a technique that shows a sequence of spot (or zero-coupon) rates consistent with the prices and yields on coupon bonds.

Variations of the zero-coupon swap exist to meet different investment needs. A reverse zero-coupon exchange pays the fixed lump-sum payment upfront when the contract is initiated, reducing credit risk for the pay-floating party. Under an exchangeable zero-coupon exchange, the party scheduled to receive a fixed sum at the maturity date can use an embedded option to turn the lump-sum payment into a series of fixed costs.

The floating payer will benefit from this structure if volatility declines and interest rates are relatively stable. It is also possible for the floating-rate payments to be paid as a lump sum in a zero-coupon swap under an exchangeable zero-coupon exchange.

Conclusion

- A zero-coupon swap involves the fixed side of the swap being paid in one lump sum when the contract reaches maturity.

- The variable side of the swap still makes regular payments, as they would in a plain vanilla swap.

- Because the fixed leg is paid as a lump sum, valuing a zero-coupon swap involves determining the present value of those cash flows using a zero-coupon bond’s implied interest rate.