What Is Whole-Life Cost?

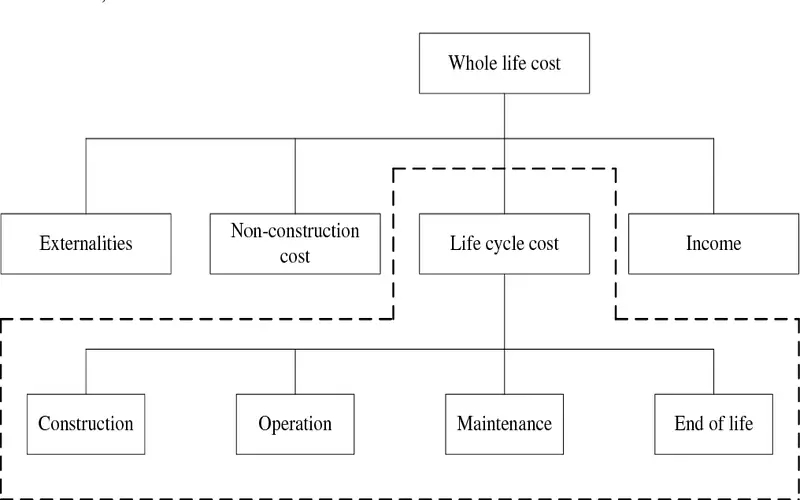

According to financial analysis, the whole-life cost is the overall cost of holding an asset for its whole life, from acquisition to disposal. Other names for it include “cradle to grave,” “lifespan cost,” and “womb to tomb.” Purchase and installation costs, construction and design expenses, running and maintenance costs, related finance costs, depreciation, and disposal costs are all included in the whole-life cost.

Whole-life cost accounting also includes expenditures associated with social and environmental impact elements, which are often disregarded. It is feasible to determine the environmental effects of producing the concrete enclosure and the water needed for copper refining in the context of building a nuclear power plant, among other things.

Even though many solutions are promoted as being “good” for the environment, a whole-life cost analysis makes it possible to determine if one alternative has a more significant or lower environmental cost.

Understanding

Whole-life cost analysis is often used when weighing alternatives for investing in new assets or doing studies to reduce whole-life costs across an asset’s lifespan. Decisions on acquisitions or between two projects may also be made using it.

When comparing investment options, a financial analyst must consider all possible future expenditures, not acquisition expenses. Most businesses overlook the longer-term costs of an asset because they are more concerned with the upfront capital expenditures of production or purchase. An asset’s return could be overstated if whole-life expenses aren’t considered. Even though an investment may have low creation costs, purchasing it might result in expensive maintenance or customer service expenses in the future.

While most short-term expenditures—and even depreciation—can be assessed or calculated, long-term costs are more difficult to quantify. Furthermore, it isn’t easy to quantify elements like the influence on the environment or society. However, compared to most other approaches, whole-life costing could provide a more realistic image of an asset’s actual cost.

A significant piece of equipment bought for manufacturing serves as an example of the need to calculate whole-life costs. Consider, for instance, a device that affixes nylon flocks to foam rubber pads used in manufacturing painting instruments. The flocking machine will need ongoing maintenance and replacement because its many components exceed the initial acquisition and installation costs. A device of this kind can pose environmental risks during cleaning or require intricate dismantling for proper disposal. A whole-life cost study is essential to determine the equipment’s long-term financial benefit from purchase and usage.

Conclusion

- The overall cost of holding an asset for its whole life, from acquisition to disposal, is known as the whole-life cost.

- Purchase and installation costs, construction and design expenses, running and maintenance costs, related finance costs, depreciation, and disposal costs are all included in the whole-life cost.

- Whole-life cost accounting also includes expenditures associated with social and environmental impact elements, which are often disregarded.

- Most businesses overlook the longer-term expenses of an asset because they are more concerned with the upfront capital expenditures of production or purchase.