The Automated Clearing House (ACH): What is it?

Nacha operates the Automated Clearing House (ACH), an electronic financial transfer system. However, the Automated Clearing House was formally founded in the middle of the 1970s, and its origins date back to the late 1960s. Payroll deposits are only one of the various ACH transaction types offered by the payment system. A credit or debit must occur on the recipient’s end, and a debit must arise from the originator.

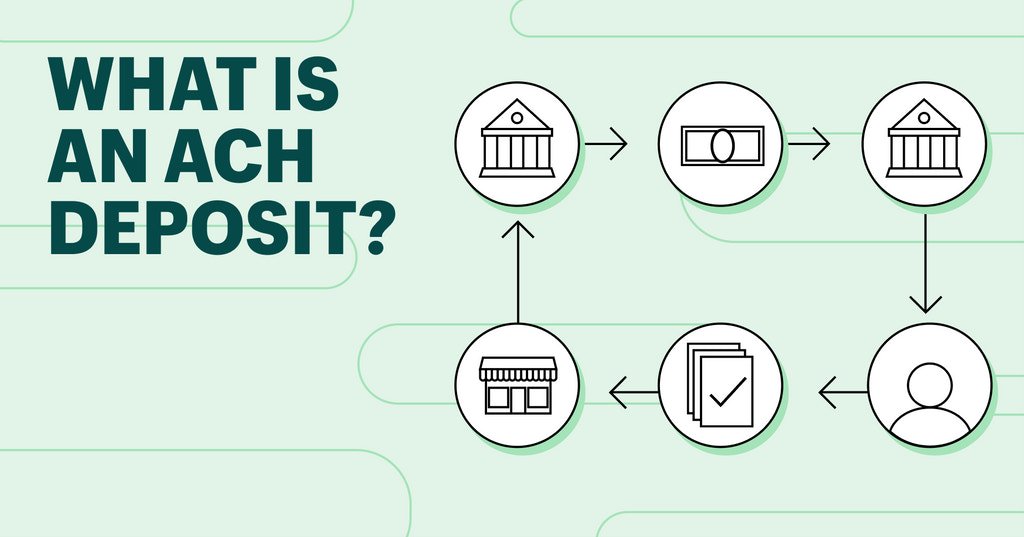

The Operation of the Automated Clearing House (ACH)

Financial institutions use the ACH Network, an electronic technology, to make financial transactions more accessible in the United States. It represents more than 10,000 financial institutions. Nearly 30 billion electronic financial transactions were made possible via ACH in 2022, bringing the total transaction value to almost $72.6 trillion. In essence, the network serves as a financial center, assisting individuals and institutions in transferring funds across bank accounts. ACH transactions include the following types of deposits and payments:

- Exchanges between businesses (B2B)

- Governmental exchanges

- Customer interactions

This is how the system functions. Utilizing the ACH network, an originator initiates a direct deposit or payment transaction using credit and debit. The originating depository financial institution sometimes called the originator’s bank, receives the ACH transaction and bundles it with other ACH transactions to be distributed regularly during the day.

An ACH operator, such as the Federal Reserve or a clearinghouse, receives the batch of ACH transactions containing the originator’s transaction from the originating institution. The receiving depository financial institution, or the intended recipient’s bank or financial institution, receives the trades once the ACH operator sorts the batch. The recipient’s bank account gets the transaction and balances the two versions to complete the process. Most ACH transactions—if not all—can be settled on the same day, thanks to changes made to NACHA’s operating standards in March 2021.

Two Particular Ideas

Nacha provides a payment system called ACH. It is an autonomous organization once known as the National Automated Clearing House Association. Although the ACH network has existed since 1968, it wasn’t formally founded until 1974.

This network develops, oversees, and enforces the rules governing electronic payments. The operational guidelines of the organization are made to make it easier for the volume and range of electronic payments made inside the network to expand.

Payroll and other direct deposits, tax returns, consumer bills, tax payments, and several other payment services both domestically and abroad are examples of ACH transaction types.

Benefits and Drawbacks of the ACH Benefits

Online transactions are speedy and straightforward because of the ACH Network, which aggregates financial transactions and executes them at certain times. According to NACHA regulations, the typical ACH credit transaction settles in one to two business days, whereas the specific ACH debit transaction settles in one business day.

The speed and efficiency of corporate and government transactions have been enhanced by deploying the ACH network to enable electronic money transfers. Through direct deposit transfers or electronic checks, people may now send money straight to one another from their bank accounts more quickly and affordably, thanks to ACH transactions.

The average time for funds to clear through ACH for individual banking services was two or three business days. NACHA implemented three phases of same-day ACH settlement beginning in 2016. Phase 3 was introduced in March 2018 and mandates that receiving depository financial institutions (RDFIs) provide the recipient access to same-day ACH credit and debit transactions for withdrawal by 5 p.m. On the settlement date of the transaction, they have to be in the RDFI’s local time and are liable to the right of return as per NACHA regulations.

The ACH network was initially limited to transactions between US accounts. This meant that you could not use this payment mechanism for any transactions intended for international transfers. International ACH Transactions (IAT), which Nacha introduced in 2021, let banks conduct cross-border business.

The drawbacks Some banking institutions may limit the quantity of money you can send. You might need to take many steps to complete a considerable transfer. For example, you might only be able to send $1,000 in financial transfers to your child at college. You must submit multiple transfers if they demand additional money for books and rent.

Certain banks levy fees for ACH transactions. There may also be a cost for each transaction. If you’re not used to handling several transactions, this might quickly build up and negatively impact your revenue.

Pros:

- Facilitates quick and straightforward online transactions

- improves promptness and efficiency

- Offers financial transactions on the same day.

- Available worldwide

Cons:

- Banks could restrict the volume of transactions.

- Costs

What Is the Process of the Automated Clearing House?

The originator initiates the Automated Clearing House (ACH) transaction by submitting a request. Their bank combines the marketing with others and sends it out throughout the day. A clearinghouse receives the batch, sorts it, and then transmits each transaction to the appropriate bank. Each receiving bank deposits the funds into the recipient’s account.

An Automated Clearing House Transaction: What Is It?

An electronic transaction that needs a debit from the originating bank and a credit to the receiving bank is an Automated Clearing House, or ACH, transaction. A clearinghouse processes transactions before combining them and sending them to the recipient’s bank. If a transaction is completed before 5 p.m., it is often carried out the same day.

Do automated clearing house transactions have any drawbacks?

ACH transactions could incur costs; this will depend on your bank. This implies that your fee expenditure will increase as you work harder. If you wish to send enormous sums of money to other individuals, you might need to make repeated transactions since certain banks limit the amount of money you can send through the system.

It used to be quite challenging to send money to someone else. However, things have gotten considerably more manageable since the invention of modern technology. The ACH, or Automated Clearing House, makes payments between banks easier. As a result, there’s no need to take money out of one account and put it into another.

The network is modified to enable same-day transaction execution for people and companies. However, remember that there are certain limitations. There can be restrictions on the amount you can move, and there might be costs. Find out from your bank how ACH transactions are handled.

Conclusion

- Payments may be made domestically and abroad with the help of the Automated Clearing House (ACH), an electronic money transfer system.

- Nacha oversees the ACH.

- Most ACH credit and debit transactions can now clear on the same working day, thanks to recent regulation changes.

- Transferring money is quick and straightforward using ACH transactions.

- Banks may charge fees and restrict the amount you can move.