What is a Barrier Option? Knock-in vs. Knock-out Options

A form of derivative known as a barrier option is one in which the payout is contingent on whether or not the underlying asset has reached or surpassed a defined price.

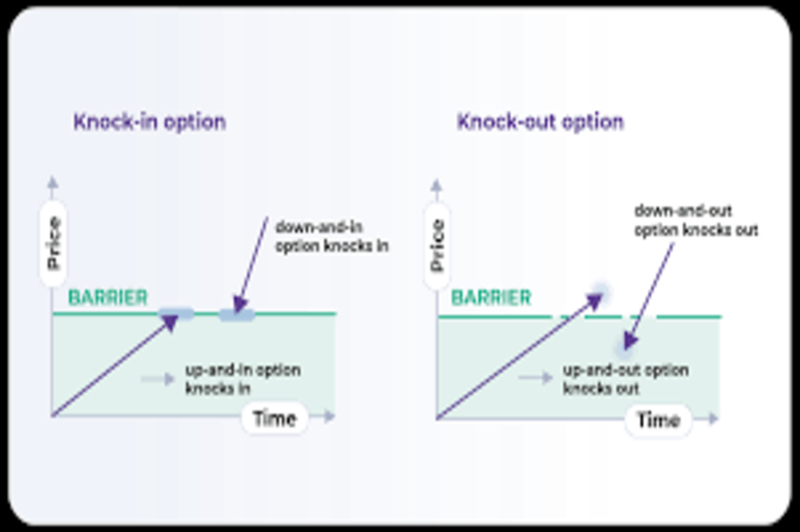

It is possible for a barrier option to be a knock-out, which means that it will become worthless if the underlying price goes over a specified threshold. This will restrict gains for the holder of the option and limit losses for the writer. Another possibility is that it is a knock-in, meaning it is worthless until the underlying asset hits a particular price.

Barrier choices are called exotic options because they are more complicated than the primary options in the United States or Europe. The value of barrier options is path-dependent because their value shifts in response to changes in the underlying value during the duration of the contract term for the option. To put it another way, the subsequent price path of the underlying asset determines the payment of a barrier option. When a specific price point barrier is crossed, the option loses all its value or becomes active.

Varieties of Obstacles Available

Generally speaking, barrier alternatives may be categorized as either knock-in or knock-out configurations.

Alternatives for Knock-in Barriers

A knock-in option is a sort of barrier option in which the rights associated with the option do not become active until the underlying asset’s price hits a certain threshold during the option’s life. This occurs only when the option is exercised. After a barrier has been knocked down or a choice has been brought into existence, it will continue to exist until it is no longer available.

There are two possible classifications for knock-in options: up-and-in and down-and-in. In a type of option known as an up-and-in barrier option, the presence of the option is contingent upon the underlying asset’s price exceeding the pre-specified barrier, which is established at a level higher than the starting price of the underlying asset. On the other hand, a down-and-in barrier option is only triggered when the underlying asset’s price falls below a predetermined barrier that is established to be lower than the original price of the underlying asset.

Other Options for Knock-out Barriers

In contrast to knock-in barrier options, knock-out barriers are rendered null and void if the underlying asset approaches a barrier during the duration of the option being issued. It is possible to categorize knock-out barrier choices as either up-and-out or down-and-out variations. The existence of an up-and-out option is terminated when the underlying security reaches a price that is higher than the barrier that was established above the starting price of the underlying. The existence of a down-and-out option is terminated when the underlying asset falls below a barrier that is defined as being lower than the beginning price of the underlying asset. There is a possibility that the option will be knocked out or terminated if the barrier is an underlying asset that reaches the barrier during the option’s life.

Options for Other Categories of Obstacles

It is possible to have further variations of the barrier choices that were explained before. All three of them are as follows:

All types of barrier options, including knock-out and knock-in barrier options, have the potential to include a clause that allows for the distribution of refunds to holders if the option does not reach the barrier price and becomes worthless. These kinds of choices are referred to as rebate barrier offerings. In situations like this, rebates are often presented as a percentage of the option holder’s premium.

Alternatives for the Turbo Warrant Barrier: The Turbo warrants are a sort of down-and-out option that is highly leveraged and is characterized by minimal volatility. They are primarily traded in Europe and Hong Kong. They have a sizeable following in Germany and are utilized for speculating.

Parisian Options: The contract is not triggered even if the barrier price is reached in a Parisian option. Instead, for the contract to take effect, the underlying asset’s price must remain above the trigger barrier price for a period that has been predetermined with consideration. Within the context of this form of option, the length of time that the price of the underlying asset spends both outside and inside the barrier price range is measured.

Options for Trade Barriers and Their Reasons

In general, barrier options have lower premiums than comparable options with no barriers. This is because barrier options come with extra conditions that are built in. Therefore, if a trader feels that the barrier is not likely to be achieved, they can choose to purchase a knock-out option, for instance, because it has a lesser premium and the barrier condition is not likely to affect them.

If an individual desires to hedge a position, but only if the underlying asset’s price hits a particular level, they may choose to utilize knock-in options. Because of the reduced premium associated with the barrier option, this may be more tempting than the non-barrier choices offered by the American or European markets.

Several Examples of Possible Obstacles

The following are two instances of the barrier alternatives that were discussed before.

The Knock-in Barrier Alternative

Consider the following scenario: an investor buys an up-and-in call option with a strike price of $60 and a barrier of $65 when the underlying stock trades at $55. The option would not become available for purchase until the underlying stock price reached a level greater than $65. However, the option will only become relevant if the underlying price hits $65, even though the investor is responsible for paying for the option, and there is a possibility that it could become valuable. If this does not occur, the option will never be exercised, and the person who purchased it will lose the money they paid.

The Knock-out Barrier Alternative

Consider the following scenario: a trader bought an up-and-out put option with a barrier of $25 and a strike price of $20 when the underlying securities were trading at $18. During the option’s duration, the underlying security experiences an increase in value greater than $25; hence, the option is terminated. Even though it just momentarily reached $25 and fell below that level, the option is now ineffective.

What Exactly Are the Exotic Choices?

The payment structure, expiration date, and striking price of exotic options differ from those of more conventional American and European options. An exotic option is a derivative contract that differs from these other options. In addition to being more complicated, exotic options provide more investment opportunities and may be tailored to the investor’s comfort level with risk and desired outcomes.

What is the Difference Between the Options Available in the United States and Europe?

An American option allows its holders to exercise their rights at any moment up until and including the day on which the option expires. The execution of a European option, on the other hand, is restricted to the day when the option is coming to an end.

In what ways are the various barrier options beneficial?

One of the most significant benefits of barrier options is that, compared to standard options, they feature cheaper premiums for the option buyer. In addition, they reduce the risk the option seller is exposed to and provide investors with greater leeway and flexibility in determining the terms of their contracts.

When the asset’s price crosses a particular price barrier, a barrier option is a form of derivative contract that is either immediately triggered or extinguished. The first and second scenarios are called knock-in and knock-out, respectively. There are also other barrier options, including Parisian options, turbo warrant barrier options, and rebate barrier options. The primary characteristic of barrier options is that the price path of the underlying asset determines the payment. Most importantly, they provide cheaper premiums for the option buyer, their primary advantage.

Conclusion

- Barrier options are a sort of exotic option in which the payoff is contingent on whether or not the option has reached or surpassed a barrier price that has been predetermined.

- Compared to ordinary options, barrier options have much lower premiums and are also utilized for hedging situations.

- In general, there are two kinds of barrier choices: knock-out and knock-in barrier options.

- By the time the price of the underlying asset exceeds a certain threshold throughout the life of the option, the rights linked with a knock-in option come into reality.

- On the other hand, a knock-out barrier option is rendered null and void if the underlying asset falls below a certain threshold within the duration of the option’s existence.