What is an Umbrella Personal Liability policy?

An umbrella personal liability insurance policy provides extra liability coverage beyond the limitations of the insured’s house, vehicle, or other liability coverage. It offers extra protection to those who may suffer significant losses if they harm another person or their property. Because umbrella insurance offers comprehensive coverage, it may cover some claims that a regular policy would not.

DISCOVERING The Unified Personal Liability Policy

Excess liability insurance is another name for umbrella personal liability insurance. If a policyholder is sued for damages, it shields savings and other assets from significant legal action. These lawsuits may go beyond the liability restrictions of a vehicle, homeowners, or other insurance policy. Umbrella insurance covers damages up to the contract’s maximum.

A policy must have minimum liability levels stipulated by the insurance provider before an individual may add umbrella personal liability to an already-existing policy. The policyholder who wishes to add umbrella coverage must have a base level of $250,000 to $300,000 for house insurance and $150,000 to $250,000 for vehicle insurance, depending on the provider.

Since there is little chance of a large claim, umbrella insurance often does not significantly increase premiums. Additionally, the rate can be lower if the policy is purchased from the same insurer as the initial house, vehicle, or boat insurance. Umbrella personal liability plans do not cover damages from criminal activity, contract disputes, or commercial losses.

Auxiliary Policies: Guard Those Who Stand to Lose a Lot

Those who are rich and face a high chance of losing money in a lawsuit would benefit most from the additional coverage provided by umbrella insurance. For instance, a motorist with $5 million in assets may be held accountable for damages beyond the $250,000 maximum on most auto insurance policies if they strike and seriously hurt a pedestrian. The motorist may also be liable for the wounded pedestrian’s lost wages and medical expenses. The driver’s money may be destroyed entirely if the pedestrian turns out to be a top earner who cannot work due to the obligation, which could quickly amount to millions of dollars.

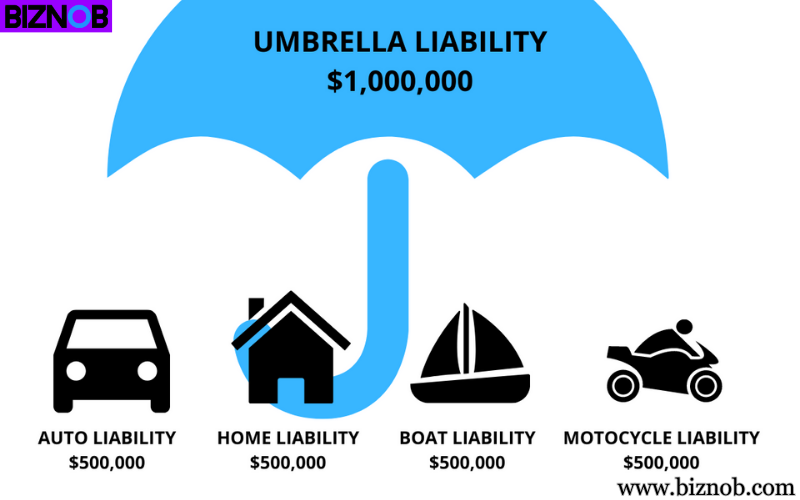

$1 million is the starting amount of umbrella coverage, increasing by $1 million each time.

It is theoretically feasible for a plaintiff to get a judgment in a case that exceeds their net worth. However, federal law severely restricts the ability to garnish earnings for civil damages. State laws differ from jurisdiction to jurisdiction regarding the asset protection they provide. For instance, some states provide the main homestead with limitless protection, others with restricted protection, and others without protection. Annuities and life insurance payouts are no different.