What exactly is mezzanine financing?

Mezzanine financing is a mix of debt and equity financing that allows the lender to convert the debt to an equity stake in the company in the event of a default, usually after venture capitalists and other senior lenders have been paid. It exists in terms of risk between senior debt and equity.

Mezzanine debt includes equity instruments. Attached are commonly referred to as warrants, which raise the value of the subordinated debt and allow for additional flexibility when dealing with bondholders. Mezzanine financing is typically related to acquisitions and buyouts, and it can be used to prioritize new owners above existing owners in the event of bankruptcy.

What is mezzanine financing?

Mezzanine finance is a high-risk loan that spans the debt and equity financing gap. It is superior to pure equity but inferior to pure debt. However, it also provides some of the best returns to debt investors compared to other types of debt, as it frequently obtains rates between 12% and 20% per year and sometimes as high as 30%. Mezzanine financing can be considered as either costly debt or cheaper equity because it carries a higher interest rate than senior debt obtained through banks but is significantly less expensive than equity in terms of the overall cost of capital. It also dilutes the company’s share value. Finally, mezzanine financing allows a company to raise more cash and boost its return on equity.

Companies will seek mezzanine financing to fund specific growth projects or to assist with short- to medium-term acquisitions. These loans are frequently funded by the company’s long-term investors and existing capital providers. There is no duty to repay the money obtained through equity financing in the case of preferred equity. Because there are no necessary payments, the corporation has more liquid capital to invest in the business. Even a mezzanine loan involves only interest payments before maturity, leaving the firm owner with additional free money.

A variety of traits are common in mezzanine loan structuring, including:

- Mezzanine debt is subordinate to senior debt but takes precedence over preferred and common stock.

- They have higher yields than regular debt.

- They are frequently unsecured debts.

- There is no loan principal amortization.

- They can be arranged with a mix of fixed and variable interest rates.

Structure of Mezzanine Financing

Mezzanine finance can be found in a company’s capital structure between its senior debt and common stock as subordinated debt, preferred equity, or a combination. Unsecured subordinate debt is the most prevalent arrangement for mezzanine finance.

Sub-debt is also known as an unsecured bond or loan that ranks lower in its ability to claim against the company’s assets or earnings than more senior loans or securities. When a borrower defaults, sub-debt holders are not paid until all senior debt holders have been paid in full. Unsecured sub-debt is debt solely backed by the company’s commitment to pay.

In other words, no lien or other credit exists to back the loan. A lien on the underlying property secures other secured mezzanine debt. Payments are often made in monthly debt service payments, depending on a fixed or adjustable interest rate and the balance due at maturity. Instead of a loan that can be unsecured or secured by a lien, preferred equity is an equity investment in a property-owning corporation. It is usually junior to mortgage and mezzanine loans but senior to common equity. Because of the heightened risk and absence of security, it is often seen as a higher risk than mezzanine debt.

Priority dividends are made before any payouts to ordinary equity holders. Some investors bargain for increased profit participation. The principal is returned on the redemption date, generally after the mezzanine debt. The sponsor may occasionally negotiate an extension of this deadline. On the other hand, a preferred stock investor may have broader corporate approval privileges because it is not subject to lender liability.

Redemption, Maturity, and Transferability

Mezzanine finance typically has a maturity period of five years or more. On the other hand, the maturity date of any specific debt or equity issue usually depends on the scheduled maturities of existing loans in the issuer’s financing structure. Preferred equity has no set maturity date and may be called by the issuer at any time after it is issued. Redemption is typically used to take advantage of decreasing market interest rates by calling in and re-issuing debt and equity at cheaper rates.

In general, the lender in mezzanine finance has unfettered transfer rights. If the loan includes future payouts or advances, the borrower may be able to negotiate a qualified transferee requirement as a transfer restriction. In contrast, preferred equity is frequently subject to restrictions or limits on transferring the purchaser’s interest in the firm. The corporation may allow transfers once 100% of the preferred equity has been committed.

The Benefits and Drawbacks of Mezzanine Financing

Mezzanine finance, like any complicated financial product or service, has advantages and disadvantages for both lenders and borrowers to consider

Advantages

Mezzanine finance may result in lenders (or investors) getting immediate stock in a business or earning warrants for future equity purchases. This can significantly boost an investor’s rate of return (ROR). Furthermore, mezzanine financing providers are contractually obligated to receive monthly, quarterly, or annual interest payments.

Borrowers like mezzanine debt because the interest they pay is a tax-deductible business expense, lowering the actual cost of the debt significantly. Furthermore, mezzanine financing is more manageable than other debt arrangements since borrowers can shift their interest to the loan balance. If a borrower cannot make an interest payment on time, some or all of the interest may be delayed. Other sorts of debt often do not have this choice.

Furthermore, rapidly expanding businesses increase in value and may restructure mezzanine financing loans into a single senior loan at a reduced interest rate, saving on interest costs in the long run. As an investor, the lender is frequently rewarded with an additional equity interest or the option to earn such an interest (a warrant). If the venture succeeds, the small add-ons can become extremely valuable. Mezzanine debt also has a substantially greater rate of return, which is essential in the current low interest-rate environment. Mezzanine debt also provides guaranteed periodic payments instead of preferred equity’s potential but not guaranteed dividends.

Disadvantages

Owners may give up some control and upside potential while obtaining mezzanine financing due to the loss of equity. Lenders may have a long-term view and want a board presence. Owners also pay higher interest as the mezzanine financing is extended. Loan agreements will frequently include restrictive covenants that limit the borrower’s ability to borrow further funds or restructure senior debt, as well as financial benchmarks the borrower must meet. Payout restrictions for essential employees and even owners are not unusual.

If the borrowing company fails, mezzanine lenders may lose their investment. In other words, when a corporation fails, senior debt holders get paid first by liquidating the company’s assets. Mezzanine lenders lose if no assets remain after the senior debt is paid off. Finally, mezzanine loan debt and equity can be time-consuming and challenging to arrange and implement. Most such transactions will take three to six months to complete.

PROS

- Debt incurred by a “patient” over a long period

- less expensive than raising equity

- structural adaptability

- There is no dilution of the company’s equity.

- Lenders are typically long-term.

CONS

- Interest rates that are too high

- Subordinated debt

- It might be difficult and time-consuming to organize.

- Additional credit restrictions may be imposed.

- The owner must give up some control.

Mezzanine Financing Example

In a mezzanine loan financing scenario, Bank XYZ lends $15 million to Company ABC, a manufacturer of surgical instruments. The financing replaced a higher-interest $10 million credit line with better terms. Company ABC increased its operating capital to help bring new items to market and paid down a higher-interest debt. Bank XYZ will receive interest payments of 10% per year and be allowed to convert the debt to an equity holding if the company defaults. Bank XYZ could prevent Company ABC from borrowing additional funds and enforce specific financial ratio rules.

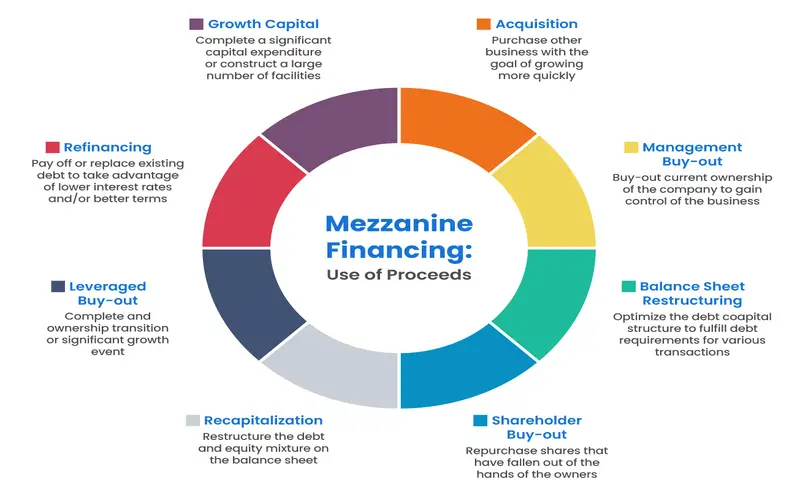

Company 123, for example, issues Series B 10% preferred stock with a par value of $25 and a liquidation value of $500. When funds are available, the stock will pay out periodic dividends until the maturity date is reached. The comparatively high liquidation value is a takeover defense that makes acquiring the stock for such purposes unprofitable. Mezzanine loan finance and preferred equity are beneficial in various situations. These are some examples:

- Existing business recapitalization

- Leveraged buyouts were used to offer funding to buyers.

- Management buyouts allow the company’s present management to purchase the company’s current owners.

- Growth capital is used for large capital expenditures or facility construction.

- Acquisition funding

- Shareholder purchasers are particularly appealing to family-owned enterprises seeking to reclaim control of shares that may have fallen out of the family’s hands to maintain or increase family control of the business.

- Existing debt is refinanced to pay it off or replace it.

- Balance-sheet reorganizations, particularly by deferring or eliminating forced repayments,

Questions and Answers

What exactly is a mezzanine loan?

A mezzanine loan is a type of capital that combines the benefits of less hazardous senior debt with more significant risk equity. Mezzanine debt is typically subordinate to senior debt, although it can also be preferred with a fixed-rate payment or divided equity. They may also have some participation rights, such as warrants, in the company’s common equity, though in a significantly less dilutive manner than the issuing of common shares.

Mezzanine loans are typically costly (in the 15% to 20% range) but are also “patient” debt in that no principal payments are needed before maturity. This debt’s patient attitude permits the company to expand toward the ability to repay the loans and increase its ability to bear more senior and, hence, less expensive debt. It is frequently both subordinated and unsecured. If the borrower runs into liquidity issues, stopping existing interest payments on mezzanine debt is possible, giving senior lenders additional confidence in their protected senior status.

What is real estate mezzanine financing?

A mezzanine loan for real estate is typically used to fund purchases or development initiatives. Within the entity’s capital structure, they are subordinate to senior debt but have priority over preferred and common equity.

Mezzanine bridge loans pay for the portion of a purchase or development project not covered by senior debt. The loans are unsecured, but in the event of a default, they may be substituted with equity. Mezzanine financing permits the borrower to raise capital without causing ownership dilution that would occur if a considerable quantity of preferred or common equity was issued.

On the other hand, real estate mezzanine loans appear as equity on the balance sheet, which may make securing further funding easier. Real estate mezzanine loans provide the lender with very high rates of return in a low-interest rate environment, the potential to earn some equity or control of the business, and, on occasion, the ability to apply some control over the business’s operations.

How Are Mezzanine Funds Profitable?

A mezzanine fund is a pool of cash that tries to invest in mezzanine finance for acquisitions, growth, recapitalization, management buyouts, or leveraged buyouts. Investors in a mezzanine fund earn a rate of return of 15 to 20%, more significant than the rate of return granted by other kinds of debt financing. Like any other pooled investment, a mezzanine fund will profit from interest on its pooled investments and from the acquisition and sale of various mezzanine financing products.

Who is the source of mezzanine financing?

Mezzanine debt is given by lenders specializing in such loans and typically have capital ranging from $100 million to more than $5 billion. They seek to make loans to businesses that can safely service more significant debt.

An excellent debt supplier would have a long track record of positive outcomes and would be willing to provide references from previous transactions. The provider should also be willing and able to tailor the debt structure to match the demands and plans of the borrower.

Finally, the ideal provider will be willing to work in your best interests, giving you the most value for the quantity, price, and flexibility of the loan raised. Often, lenders have previously worked with the company seeking the loan, and each has firsthand knowledge of the other’s dependability and understanding of the business at hand.

Are mezzanine loans guaranteed?

Unsecured mezzanine debts can be secured. Real estate uses are frequently indirectly secured to some extent by the borrower’s real estate holdings. The debt in corporate mezzanine financing is secured by the borrower’s ownership interest in the company; however, this is because a mezzanine loan is relatively low on the repayment schedule. This “collateral” could be of limited worth.

Conclusion

- Mezzanine financing combines debt and equity financing that allows businesses to raise capital for specialized projects or assist with acquisitions.

- Mezzanine lending is also employed in mezzanine funds, pooled investments that provide mezzanine financing to highly qualified enterprises, similar to mutual funds.

- Compared to traditional corporate debt, this financing can deliver more generous returns to investors, frequently paying between 12% and 20% per year.

- Mezzanine loans are typically used to expand existing businesses rather than as start-up or early-stage financing.

- If the market interest rate falls sufficiently, mezzanine and preferred equity funding may be called in and replaced by lower-interest borrowing.