What Is a Liquidity Trap?

Even at low interest rates, consumers and investors may hoard cash instead of using it for investments or spending, creating a liquidity trap that hinders policymakers’ ability to promote economic growth.

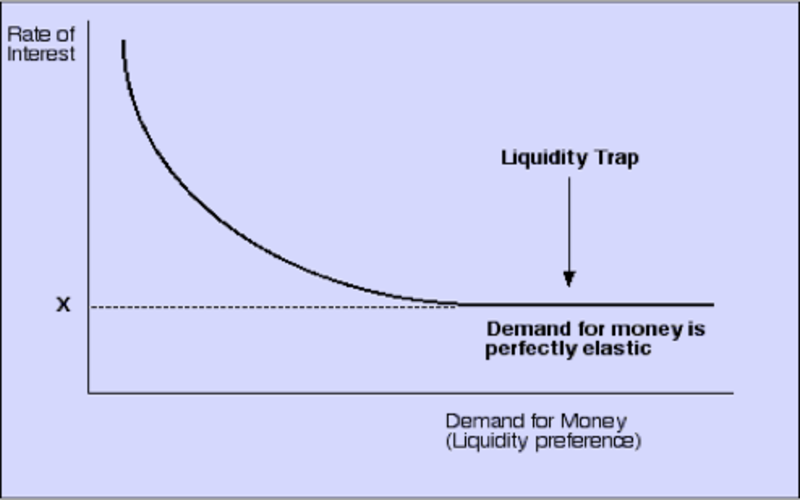

Economist John Maynard Keynes used the phrase “liquidity trap” to describe a situation in which interest rates dropped so that most people would hold cash rather than invest in bonds and other debt instruments. Keynes claimed that the outcome would be that monetary authorities could not reduce interest rates further or expand the money supply to promote growth.

A liquidity trap may form when investors and consumers hold cash in checking and savings accounts because they think interest rates will rise shortly. Bond prices would decline, making them a less desirable choice.

Since Keynes’ time, the term “liquidity trap” has gained more popularity to describe a situation in which widespread cash hoarding as a result of impending bad news causes weak economic growth.

Knowing What a Liquidity Trap Is

Excessive consumer savings, frequently prompted by the anticipation of unfavorable economic development, can render monetary policy largely futile.

The central bank cannot lower interest rates if they are already at or near zero. It wouldn’t work if the amount of money in circulation increased. People don’t need any more motivation because they are already saving money.

Crucial is the belief in a terrible future event. Bond prices will decline, and rates will rise when investors hoard cash and sell bonds. Bond prices are declining, and customers are not interested in purchasing bonds despite rising yields. Instead, they would store cash at a lesser yield.

One prominent issue with a liquidity trap is that banks struggle to find eligible customers to lend to. This is made worse because there isn’t much space for extra incentives to draw in well-qualified applicants, given that interest rates are already so close to zero.

This lack of desire to borrow money is seen in many areas of the economy, including business, home, and auto loans.

Indices of an Overdraft Situation

A sign of a liquidity trap might be found in low interest rates. Low interest rates impact bondholder behavior, particularly when combined with worries about the country’s current financial situation. Bonds are eventually sold at a price that is detrimental to the economy.

On the other hand, customers tend to hold their money in savings accounts with minimal risk. A central bank that raises the money supply does so with the justifiable hope that some additional funds will find their way into bonds or other assets with better yields.

However, in a liquidity trap, it just disappears into cash accounts.

A liquidity trap cannot be defined by low-interest rates alone. In addition, there must be a shortage of bondholders who want to hold onto their bonds and a restricted number of buyers for the scenario to be considered. Instead, investors are giving strict cash savings a higher priority than buying bonds.

Qualities of an Equilibrium Trap

When businesses, investors, and consumers hoard cash, the economy becomes resistant to measures taken by policymakers to promote economic activity. This phenomenon is known as a liquidity trap.

The primary attributes of a liquidity trap are as follows:

- Meager interest rates—nearly 0%

- Economic downturn

- high amounts of personal savings

- Deflation or low inflation

- Expansionary monetary policy gone wrong

Reasons Behind Liquidity Traps

The occurrence of liquidity traps is uncommon. Economists have proposed several causes or factors that may precede one.

Inflation

When prices decline, and money’s purchasing power rises, this is known as deflation. It happens less frequently and is the opposite of inflation.

Deflation may begin when individuals decide to save their money rather than use it for investments or purchases because they think prices will keep dropping. When an expensive item will cost less in a month and even less in two months, why buy it now?

In severe circumstances, a deflationary spiral may occur, in which falling prices prompt reductions in demand, production, and wages, further lowering prices.

In this kind of feedback loop, a liquidity trap may appear.

Financial Statement Downturn

An economic downturn, known as a “balance sheet recession,” is primarily the result of businesses and individuals opting to settle their debts rather than increase their spending or borrowing.

This occurs when the amount of outstanding debt increases, and lenders and borrowers are anxious that the loan might not be repaid in full.

Debt repayment precedes new loans and investments, even when interest rates decline.

A shortage of investor demand

Companies issue stock and bonds to raise money. Lower interest rates won’t make a difference if investors don’t have much demand to invest in them.

Furthermore, companies and investors may decide to delay taking any action because they see the investment as dangerous during a recessionary period of generally low demand.

Unwillingness to Lend

If banks consider the credit environment as a whole to be high-risk, they may become reluctant to lend.

Following the 2008 financial crisis, many banks experienced liquidity problems due to high subprime loan defaults. In response, the banks drastically reduced their overall loan volume.

Banks tightened their underwriting standards and turned away all but the best-qualified customers, making it impossible for many consumers and businesses to get loans—even at meager interest rates.

Resolving the Trap in Liquidity

Specific, well-tried economic remedies are ineffective when applied to a liquidity trap. Sometimes, governments will purchase or sell bonds to influence interest rates, but in such a situation, buying bonds doesn’t help much because investors are too eager to sell them. It gets more challenging to get yields to go up or down and harder to get customers to take advantage of the new rate.

There are several methods for escaping a liquidity trap. While none of these might be completely effective, they might push people to start investing and spending money rather than saving it.

- A rise in the rate. The Federal Reserve may increase interest rates to encourage more investment rather than storing up personal savings. Yet, this is a challenging course of action when there is low inflation and a recession.

- A significant decrease in cost. When genuine deals are available, individuals find it impossible to resist spending money. The allure of reduced costs grows too strong, and the savings are utilized to benefit from those reduced costs.

- A rise in public expenditures. Government initiatives can stimulate expenditure and the creation of jobs when businesses hold back.

- QE, or quantitative easing. The central bank can start purchasing longer-dated government bonds and other securities like mortgage bonds to drop interest rates below zero and promote economic expenditure artificially.

- Policy of negative interest rates (NIRP). Following the global financial crisis in 2008, Europe and Japan employed this remarkable monetary policy weapon. Negative interest rates, which credit interest to borrowers and subtract interest from them, are imposed when nominal interest rates fall below zero.

It is hard to convince scared customers to spend money instead of saving it. As such, some endeavors might succeed in theory but fall short in practice.

An Actual Liquidity Trap Example

In the 1990s, Japan found itself in a liquidity trap. Despite the ongoing decline in interest rates, investment did not increase. Japan experienced deflation during the 1990s, and as of 2022, its interest rate is still negative at -0.1%.

The primary stock index in Japan, the Nikkei 225, dropped from a peak of more than 38,000 in December 1989 and is still much below that record as of early 2023. In August 2022, the index reached a multi-year high of around 29,000 before collapsing to roughly 27,500 in the same month.

Japan’s central bank placed interest rates at zero percent, but after the crisis’s peak, investment, consumption, and inflation all stayed muted for several years.

The Liquidity Trap Theory’s detractors

Liquidity traps are not believed to exist by adherents of the prominent Austrian economist Ludwig von Mises, who was a strong proponent of free-market capitalism and a fierce opponent of socialism and interventionism in the 20th century.

They conclude that, in contrast to common belief, the actions implemented by governments and central banks to combat the liquidity trap pose a more significant threat to the world’s leading economies than the liquidity trap itself.

They contend that these policies merely erode the savings pool, obstructing the possibility of a long-term economic recovery and maintaining the liquidity trap. They contend that negative interest rates are unlikely to help large economies escape a liquidity trap if the savings pool is difficult.

Is the US currently in a liquidity trap?

Early in 2023, rising interest rates and inflation were plaguing the US economy. These might cause issues, but not in a way that could result in a liquidity trap.

A liquidity trap is, by definition, limited to times when interest rates are meager. Put another way, despite the central bank’s forced reduction of loan rates to extremely appealing levels, investors, companies, and consumers are not reacting. They maintain their cash reserves.

Has there ever been a liquidity trap in the US?

Perhaps it’s hard to get two economists to agree on the existence or non-existence of a liquidity trap.

When did the stock market plummet?

Significantly, at the beginning of the COVID-19 epidemic, concerns about the economy’s capacity to withstand the shock to the system grew. Some economists argue that the United States found itself in a liquidity trap momentarily. The Federal Reserve’s M1 number, which gauges the total amount of cash in the economy, sharply increased in mid-2020, which had an impact on this outcome.

If one existed, the crisis subsided as soon as the Fed reacted by boosting liquidity and implementing quantitative easing measures.

After the 2008 financial crisis, the United States was believed to have momentarily experienced a liquidity trap as output declined and interest rates effectively went to zero. The banks refused to lend money once the housing bubble crashed, shocking investors into cashing their investments.

Following multiple rounds of stimulus expenditure by the government and quantitative easing by central banks, the US economy started to pick up steam.

Is a recession and a liquidity trap the same thing?

A recession may have a liquidity trap as one of its contributing factors. Instead of investing or spending their money, people save it. They are not persuaded to spend more by low interest rates. Monetary authorities cannot resolve the issue using their standard tool of cutting interest rates since these rates are already at or close to zero. When the market for products and services contracts and businesses reduce output and employment, this could turn into a recession.

What Makes People Stockpile Money in a Liquidity Trap?

People may hoard funds for various reasons, including a lack of faith in their ability to invest and generate a higher rate of return. They might be waiting for better deals, whether investing or spending their money, because they think deflation—or declining prices—is imminent. They might also be afraid of impending financial difficulties, either in their own lives or in the economy.

Any of the ideas above can come to pass if enough people hold them true.

Some of these individuals may wish to borrow money. Still, they will discover that lenders are hesitant to give credit at such low interest rates to anyone but the best-qualified applicants.

Is there a liquidity trap?

Strict definitions of a liquidity trap make central bank policies useless. But when more moderate approaches fail, research from economists at the Bank for International Settlements (BIS) indicates that alternative monetary policy tools like quantitative easing and negative interest rates can be helpful.

According to a working paper by the BIS titled “Does the Liquidity Trap Exist?” alternative approaches effectively managed liquidity traps in the Eurozone, Japan, and the United States. The article contends that “in such a view, the central bank’s inability to lower the short-term interest rate is irrelevant, provided that it can ramp up credit supply and if at least some non-financial economic agents are credit-constrained.”

The Final Word

A situation where savings are substantial and interest rates are shallow is known as a liquidity trap. Put another way, despite the lure of interest rates at or near zero percent, people and businesses hang onto their cash.

Since interest rates are currently zero, a liquidity trap is supposed to significantly reduce the efficacy of expansionary monetary policy.

Conclusion

- Central banks like the Federal Reserve force interest rates lower to promote spending and boost economic activity.

- When interest rates are meager, customers prefer to retain cash rather than spend or invest their money in higher-yielding bonds or other investments, known as a liquidity trap.

- In such circumstances, the central bank’s primary tool has proven ineffective.

- Fear of future economic difficulties, personal or general, is a significant cause of this syndrome.

- The impacts of a liquidity trap are not restricted to the bond market. Consumers are also spending less on products and services.