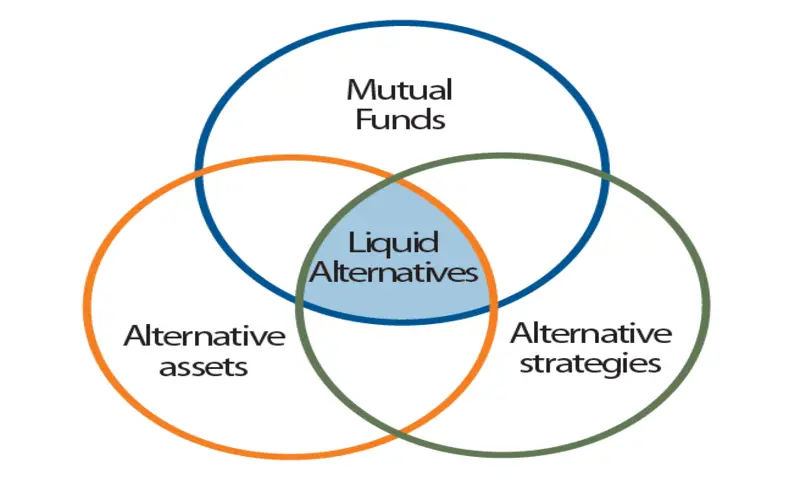

What are liquid alternatives?

Mutual or exchange-traded funds (ETFs) that offer exposure to alternative investment methods to give investors downside protection and diversification are liquid alternative investments or liquid alts. Unlike traditional alternatives that offer monthly or quarterly liquidity, the selling point of these products is that they are liquid, meaning that they may be bought and traded daily. Unlike traditional hedge funds, they offer smaller minimum commitments and don’t require investors to meet specific income or net-worth thresholds to participate.

Since most capital invested in liquid alternatives entered the market during the post-financial crisis bull market, critics contend that the liquidity of these assets will only withstand some of the challenging market conditions. Additionally, some argue that the costs of liquid substitutes are excessive. However, proponents argue that because liquid alts make hedge fund tactics more accessible to regular investors, they are a positive innovation.

Knowing What Liquid Alts Are

By giving investors access to alternative investments through daily redeemable products akin to mutual funds, liquid alts seek to mitigate the disadvantages of alternative investing.

The term “alternative investment” is ill-defined and, in theory, may apply to nearly any asset that isn’t a stock or bond intended for long-term investment. Hedge funds, real estate, distressed debt, commodities, fine art, and derivatives are a few examples. The lack of liquidity in any of these assets is a disadvantage. A $5,000 position in Alphabet Inc. is simple to dump in milliseconds without impacting the price under typical market conditions. Selling an alternative investment may need a lot more time and work, and there might be lock-up periods—even if the private equity market is booming. Additionally, making a modest investment in alternative assets could be more challenging.

Liquid Alternatives Critiqued

Since the financial crisis in 2007, the number of liquid alternative funds has increased dramatically due to the growing desire of advisors and ordinary investors to use hedge fund-like methods to guard against downside risk. According to a July 2015 study by Barron’s and Morningstar, 63% of advisors intended to allocate more than 11% of their portfolios to liquid alternatives over the following five years.

Since then, though, the liquid alternative assets market has experienced a wave of fund closures and consolidations, which has caused the sector’s growth to stall. As of the end of 2015, the market’s assets had grown to $192 billion. The market has continued to have uneven asset growth; according to Strategic Insight, liquid alternative assets increased from $179 billion at the end of 2015 to $184 billion at the end of the third quarter of 2017.

Opponents point out that costs for liquid alternative funds are typically greater than those for other actively managed mutual funds. Second, cramming otherwise illiquid assets into liquid packaging might not work well. Investors in hedge funds typically consent to withdraw money just once a quarter or once a year. Liquid alternatives have gained appeal because they are easy to trade in and out of, but if a downturn causes a run on the funds, providers would be compelled to liquidate assets at steep discounts, which could hurt investors.

Liquid Alternative Strategies and Sub-Category Examples

Morningstar has recognized twelve categories as liquid alternative methods. The biggest at the time, making up more than 80% of the funds, were as follows:

- Long-short equity refers to funds that focus on equity securities and derivatives and mix long bets with short bets made via short stock positions, options, or ETFs. The macro outlook for the fund will determine how evenly distributed short-to-long positions are.

- Nontraditional bond: These funds invest in bonds in nontraditional ways, frequently aiming for returns that aren’t tied to the bond market. “Unconstrained” funds have a lot of latitude when making investments; they might take stakes in foreign debt with high yields, for instance.

- Market neutral: Funds that aim to reduce systemic risks resulting from an excessive amount of exposure to particular industries, nations, currencies, etc. They aim to attain low beta by matching long and short positions within these domains.

- Managed futures: These funds mostly make investments using derivatives, such as foreign exchange contracts, swaps, options, and listed and over-the-counter futures. While some adopt mean-reversion or other tactics, the majority employ momentum techniques.

- Multialternative: These funds blend various alternative approaches, like the ones mentioned above. Depending on changes in the market, they could adjust their tactics or have predetermined allocations for specific strategies.

Bear-market, multi-currency, volatility, and trading-leveraged commodities (which comprise a single fund) are other categories. Citi has listed three distinct mutual fund structures under liquid alternatives: single-manager, multi-alternative, and commodities (or managed futures) funds. In the meantime, Goldman Sachs has developed an alternative set of classifications that more closely resemble hedge fund tactics. Goldman has separated its pool of liquid alternative funds into five categories: multi-strategy, event-driven, tactical trading/macro, equity long/short, and relative value.

Conclusion

- Alternative investment instruments, known as liquid alternatives or alts, are designed to be more accessible to regular investors.

- While they employ many of the same market methods, liquid alts are significantly more liquid than hedge funds, allowing investors to quickly purchase and sell shares in the fund. Liquid alts have lower investment minimums as well.