What is the Life-Cycle Hypothesis (LCH)?

An economic theory known as the life-cycle hypothesis (LCH) explains how people save and spend money throughout a lifetime. According to the hypothesis, people try to balance their lifetime consumption by saving during high income and borrowing during low income. In the 1950s, economist Franco Modigliani and his pupil Richard Brumberg developed the idea.

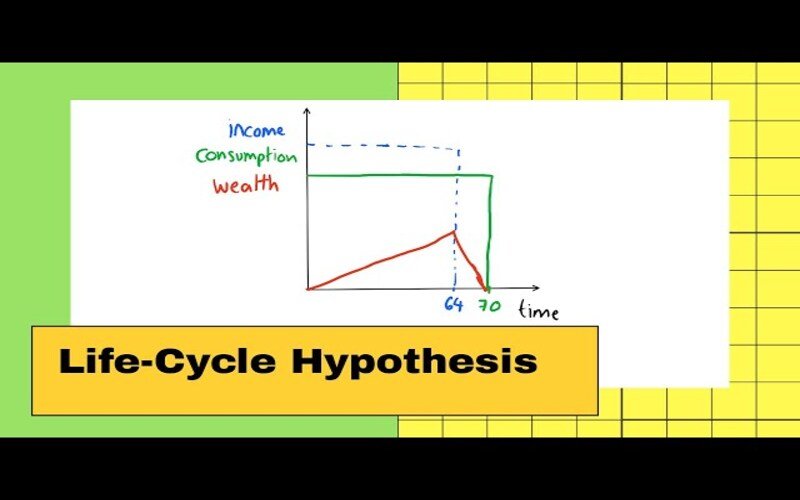

Comprehending the Life-Cycle Theory

The LCH assumes that people budget their money throughout their lives while accounting for potential future earnings. As a result, they take on debt when they are young, believing that their future earnings will allow them to repay it. They then start saving in their middle years so that when they retire, they can continue to live the same lifestyle.

Thus, a spending graph over time for an individual reveals a hump-shaped pattern, with wealth growth being lowest in youth and old age and highest in middle life.

Keynesian Theory vs. Life-Cycle Hypothesis

John Maynard Keynes, an economist, created an earlier theory in 1937 that the LCH superseded. Keynes thought that saving was merely another good and that as people’s incomes increased, so did the percentage of their savings. This suggested that if a country’s earnings increased, there would be a savings glut, which would cause aggregate demand and economic activity to stagnate. This posed a possible dilemma. The fact that Keynes ignored changes in people’s purchasing patterns over time is another issue with his theory. For instance, a middle-aged person heading a family will need more than a retiree. Although later studies have mainly confirmed the LCH, it still has issues.

Extra Thoughts on the Life-Cycle Hypothesis

The LCH presupposes various things. For instance, the theory assumes that people lose money as they age. However, wealth is frequently passed down to children, or older people may refuse to spend their money. The idea also presumes that people plan to accumulate wealth. However, many people put things off or need more self-control to save money. The idea that people make the most significant money when they are of working age is another one. When they get closer to retirement age, some people opt to continue working part-time after choosing to work less when they are still relatively young.

This implies, among other things, that younger people are more willing to take on financial risks than older ones, which is still a common belief in personal finance.

Notable additional presumptions include the idea that people with higher incomes are better at saving money and handling money than people with lower incomes. Credit card debt and poor disposable income are typical among low-income people. Finally, because older folks expect a more significant social security payment upon retirement, safety nets or means-tested payments may deter people from saving.

Conclusion

- The Life-Cycle Hypothesis (LCH) is an economic theory proposed in the early 1950s that people plan their spending over their lifespan, considering their future income.

- A graph of the LCH demonstrates a hump-shaped pattern of wealth accumulation, with low accumulation during youth and old age and significant accumulation during middle age.

- One result is that younger people are more willing to accept investing risks than older people, who must draw down their assets.