What is the LIBOR curve?

The LIBOR curve is a graphic representation of the London Interbank Offered Rate, or LIBOR, term structure for various maturities. Large banks with excellent credit ratings lend to one another at the Libor or short-term floating rate. The LIBOR curve represents the yield curve for LIBOR rates less than a year. In 2020, the secured overnight financing rate (SOFR), among other benchmarks, replaced LIBOR as the primary measure.

The LIBOR Curve: An Understanding

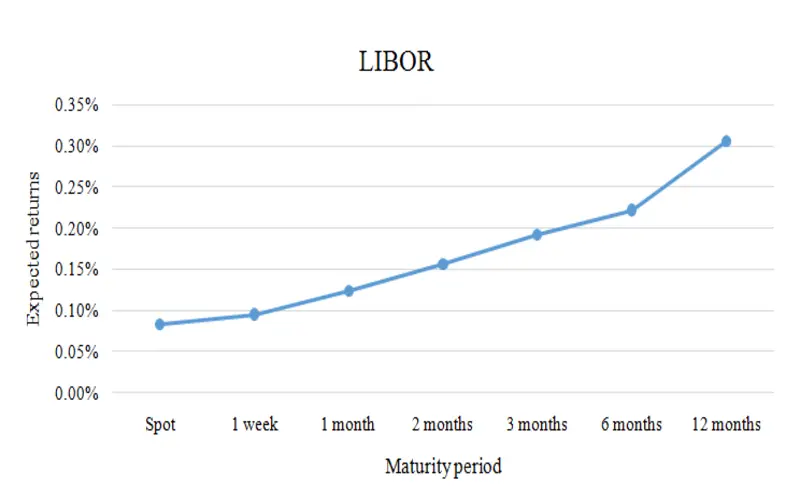

LIBOR is one of the most popular choices globally as a benchmark for short-term interest rates. The London interbank market is the leading indicator of the average interest rate that participating banks can pay for short-term loans. Plotting rates against respective maturities is done on the LIBOR curve. One week, one month, two months, three months, six months, and twelve months are the seven various maturities over which the LIBOR curve typically plots its yield curve.

A yield curve is called an interest rate curve, representing the yields of bonds with similar credit ratings but different maturity dates. Examining the yield curve’s slope can predict future interest rate movements and economic activity. Standard yield curves have an upward slope, inverted yield curves have a downward slope, and flat yield curves are in between.

Long-term rates are higher than short-term yields in an upwardly sloping market. The yield curve’s “normal” slope, which is this one, indicates an expansionary economic environment.

Short-term yields are more significant than long-term yields in an upward-sloping yield curve. Referred to as an “inverted” yield curve, it indicates that a weak economic period is either approaching or has already begun.

Flat: the short- and long-term yields mainly do not differ. There are several indicators of market uncertainty over the trajectory of the economy.

While LIBOR isn’t risk-free, it’s a reliable benchmark for assessing the trade-off between risk and return for other short-term floating-rate products. The pricing of interest rate swaps heavily relies on the LIBOR curve, which can forecast longer-end interest rates.

The LIBOR curve has drawn criticism.

Following the 2008 global financial crisis, misuse of the LIBOR system for private advantage was discovered. People who worked at contributing banks were able to alter LIBOR rates due to massive disruptions in the global financial industry. In 2013, the Financial Conduct Authority (FCA) took over LIBOR regulation in the United Kingdom. The Sterling Overnight Index Average (SONIA) was to replace the LIBOR system, which was scheduled to be phased out by 2023 as of December 2020.

Conclusion

- The LIBOR curve is a graph that shows the yield curve for different short-term LIBOR rates.

- For example, the secured overnight financing rate (SOFR) became a new standard in 2020, replacing LIBOR.

- The terms of these LIBOR rates run from one day to several months.

- The LIBOR curve shows how loan rates are likely to change in several debt markets over the next few to twelve months.