What Is a Leveraged Loan?

Leveraged loans are extended to businesses or individuals with substantial debt loads or a weak credit history. Due to the increased risk of default that lenders attribute to leveraged loans, the borrower incurs a more significant expense when obtaining one.

Generally, the interest rates on leveraged loans for individuals or organizations in debt are higher than those on conventional loans. The elevated risk associated with loan issuance is reflected in these rates.

Comprehending Leveraged Lending

At least one investment or commercial bank is responsible for arranging, administering, and structuring a leveraged loan. Arrangers may later engage in syndication, in which they transfer the loan to other banks or investors to lessen the lending institutions’ risk.

The definition of a leveraged loan lacks predetermined rules or criteria. A spread for some market participants determines it. Many loans, for instance, are subject to a floating interest rate, frequently determined by a benchmark such as the Secured Overnight Financing Rate (SOFR), which supplanted the London Interbank offered rate (LIBOR) in June 2023 or another comparable metric in addition to a stated basis or ARM margin. Typically, the credit spread adjustment increases basis points in the loan interest rate to offset SOFR depreciating below LIBOR.

A loan is classified as leveraged if the ARM margin exceeds a specified threshold. An alternative approach is to classify loans according to the borrower’s credit rating. Investment-grade loans are designated as Ba3, BB-, or lesser by the credit rating agencies Moody’s and S&P.

Price flexibility refers to the customary allowance for banks to modify loan terms during the syndication process. Through an “upper flex” process, the ARM margin may be increased if demand for the loan is inadequate at the initial interest rate. In contrast, reverse flex refers to reducing the spread over SOFR if loan demand is substantial.

What are the applications of leveraged loans by businesses?

Corporations generally employ leveraged loans to finance various objectives, such as recapitalizing the balance sheet, financing mergers and acquisitions (M&A), or refinancing debt. An example of a possible M&A structure is a leveraged buyout (LBO). The purchase and subsequent privatization of a public entity by a corporation or private equity firm constitutes an LBO. Debt is commonly employed to finance a proportionate amount of the acquisition cost. Recapitalization of the balance sheet: When a company modifies the composition of its capital structure via the capital markets, issuing debt to repurchase shares or pay dividends, which are monetary payments made to shareholders, is a typical transaction.

An Instance of a Leveraged Loan

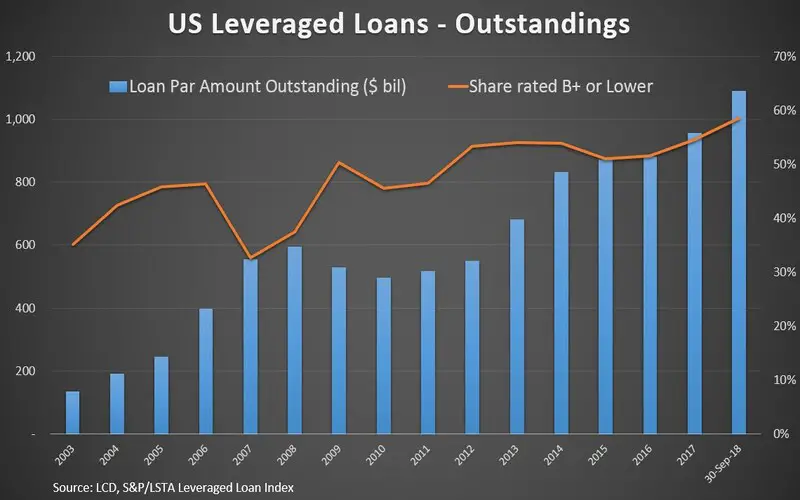

Leveraged Commentary & Data (LCD), a provider of news and analytics on leveraged loans, includes a loan with a BB- or lower rating in its universe of leveraged loans.

Alternatively, the loan is frequently classified as leveraged if a first or second lien is used to secure a nonrated, BBB-, or higher loan.

Leveraged loans are what?

The borrowers of a leveraged loan are those who have substantial debt or a poor credit rating. Lenders deem leveraged loans to entail an above-average risk of default, which pertains to the borrower’s potential inability to repay the loan. As a result of the increased risk associated with these loans, lenders typically demand higher interest rates.

What differentiates a leveraged loan from a bank loan?

Bank- or other financial institution-made leveraged loans, alternatively referred to as bank loans or floating-rate loans, are subsequently offered for sale to investors. Businesses may use the funds to finance projects, fund mergers and acquisitions, or refinance debt. The credit ratings of the organizations that obtain these loans are generally below investment grade. The borrower’s real estate and equipment as well as intellectual property like brands, trademarks, and customer records serve as collateral.

How do funds invest in leveraged loans?

Leveraged loans might be included in their portfolios depending on the investment funds’ investment strategy (including exchange-traded funds and mutual funds, or ETFs). As part of a diversified portfolio, some funds might allocate a modest amount of capital towards leveraged loans, whereas others might make substantial investments. Because the increased interest rates on these loans could result in a greater return for fund investors, fund portfolio managers might be inclined to acquire them.

Bottom Line

Individuals or organizations with substantial debt loads or a weak credit history are eligible for leveraged loans. Lenders assess the default risk associated with leveraged loans as more significant and consequently impose higher interest rates on these loans than conventional loans. This pricing structure is intended to mirror the heightened risk involved in issuing such loans.

Conclusion

- Individuals or businesses with debt or bad credit can get a leveraged loan.

- Creditors see a higher chance of failure with leveraged loans, so they charge higher interest rates to the clients.

- Because there is more danger in giving out leveraged loans, the interest rates are higher than for regular loans.