What is Level-Premium Insurance?

Permanent or term life insurance with a level premium in which the premium remains constant for the duration of the policy. Thus, premiums for this form of coverage will remain constant for the duration of the contract. A permanent insurance policy, such as a whole life, increases coverage over time.

Consequently, the coverage may be beneficial for an extended period of time. While the policyholder continues to make a fixed payment, they gain access to augmented death benefit coverage as the policy matures.

Term policies also frequently have a level premium; however, the overage amount remains constant and does not increase. Term lengths of 10, 15, 20, and 30 years are prevalent, contingent upon the policyholder’s requirements.

The Operation of Level-Premium Insurance

Premiums for level-premium insurance remain constant throughout the policy’s duration. This refers to the duration of the term (e.g., twenty or thirty years) for a term policy and until the insured dies for a permanent policy.

Expense for Premiums

Generally speaking, level-premium policies have a higher initial cost than annually renewing life insurance policies with a one-year term. However, level-premium payments are frequently more economical in the long haul. This is because, historically, an increase in coverage has compensated for the higher premiums, particularly when policyholders experience more medical issues.

Phases and Ages

The premium paid on a policy is proportional to the policyholder’s age and health; the younger and more robust the policyholder, the lower the premium level. Additionally, term life insurance premiums will vary by policy duration; longer-dated policies will incur higher monthly costs than shorter policies. The individual’s unique needs frequently determine the length of a term policy. A 20-year level premium, for instance, might be suitable if the death benefit’s primary objective is to provide income to support very young children and finance college expenses. However, if these children have already reached the early adolescent years, a ten-year premium may be adequate. All else being equal, the premiums for the 10-year term policy would be less expensive than those for the 20-year policy if the insured is the same age.

Comparing Decreasing Term Life Insurance and Level-Premium Term Insurance

A benefit is paid by level-premium term life insurance if the person dies within a specified period (the insurance term). Failure to meet the specified term timeframe will result in the non-payment of the compensation.

Similar to how a mortgage repayment decreases, decreasing-term life insurance provides less coverage over time. Typically, decreasing-term life insurance is acquired to settle a designated debt, such as a mortgage repayment. The policy guarantees that the repayment mortgage (or another designated debt) is settled in the event of mortality.

An additional specialized life insurance category is “over 50s life insurance,” which is designed specifically for individuals aged 50 to 80. Additionally, mutual life insurance involves the purchase of individual policies by two individuals in a relationship. On a first-death basis, the policy typically covers both lives. Level-Term Life Insurance Premiums

- Benefit of death for a specified period

- More affordable than a whole life

- Suitable for particular life phases and ages

- There is no benefit to the policyholder’s demise occurring after the specified period.

- It may not provide coverage for the policyholder for their lifetime.

An instance of level-premium protection

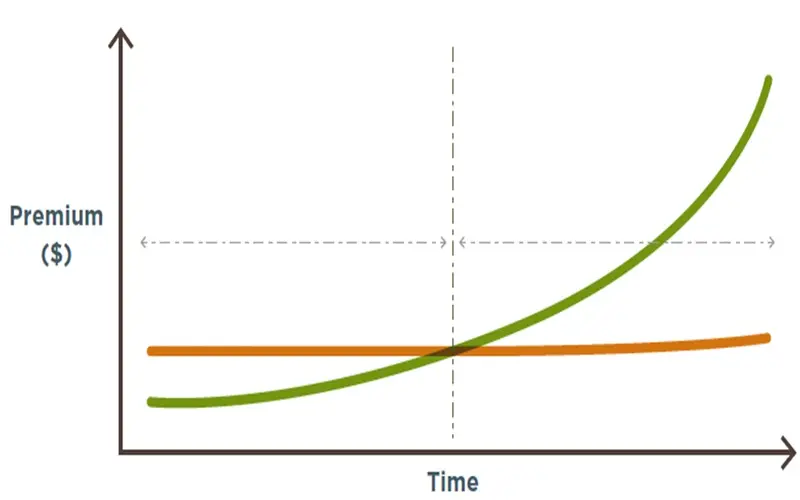

Age and duration of coverage are critical determinants in assessing the suitability of a guaranteed, level-premium policy as opposed to an annual renewable term (ART) policy, in which the premium rises with the policyholder’s age.

Consider the case of two healthy 30-year-old female acquaintances, Jen and Beth, who purchase life insurance. They each request coverage of $1 million over a thirty-year term.

For a total of $500 per year, Jen purchases a guaranteed level-premium policy for approximately $42 per month with a 30-year horizon.

Beth, however, doubts that she will require a plan for the next three to five years or until her current obligations are entirely repaid. Conversely, she purchases a yearly renewable term (YRT) policy with a monthly premium of $20 that increases by 20% annually. Thus, she pays $240 annually in year one and approximately $500 annually by year five. During years two through five, Beth paid an average of $357 per year for the same $1 million in coverage, while Jen continued to pay $500 monthly. By the time Beth reaches her fifth year and no longer requires life insurance, she will have significantly accumulated savings compared to the amount Jen spent. However, should Beth continue to believe that she requires an additional 25 years of life insurance coverage, she will gradually place herself in a reduced position. As Beth ages, she is subject to progressively increasing annual premiums. Jen, meanwhile, will maintain her annual payment of $500.

What is the operation of level-premium insurance policies?

Insurers can offer level-premium policies by, in essence, “overcharging” for the initial years of the policy, collecting funds over what is actuarially required to cover the insured’s mortality risk during that period. The additional premiums are applied to future years when the insured poses a greater risk.

Historically, which categories of policies fall under level-premium contracts?

Level-premium insurance is commonly linked to whole-life or term insurance policies, wherein the premium is assured to remain constant. Additional types of insurance, such as annual terms or variations of universal life (UL), may experience fluctuations in premiums due to evolving circumstances.

Why do permanent insurance premiums exceed those of term insurance?

Permanent insurance premiums, such as those for whole life, are greater than those for term life for two primary reasons. The first is that the policy provides perpetual life coverage for the policyholder. The second is that a cash contribution towards a permanent life premium can be withdrawn while the policyholder is still alive.

Conclusion

- Life insurance with a level rate means that the fees stay the same over the term of the policy, but the amount of coverage goes up.

- Policies with a level payment can be either fixed or term.

If you have permanent insurance, like whole life with level premiums, the death benefit will usually go up over time, even if your payments stay the same. - There is a cash value that grows with fixed life insurance, which adds to the death benefit amount.

- There are set terms for 10, 15, 20, and 30 years for term life insurance. The coverage does not increase over time.