Critical Rate Duration: What Is It?

The key rate duration quantifies the variation in the value of a debt security or a portfolio of debt instruments, usually bonds, at a given yield curve maturity point. The critical rate duration is used to quantify how sensitive the price of a debt security is to a 1% change in yield for a given maturity while holding other maturities constant.

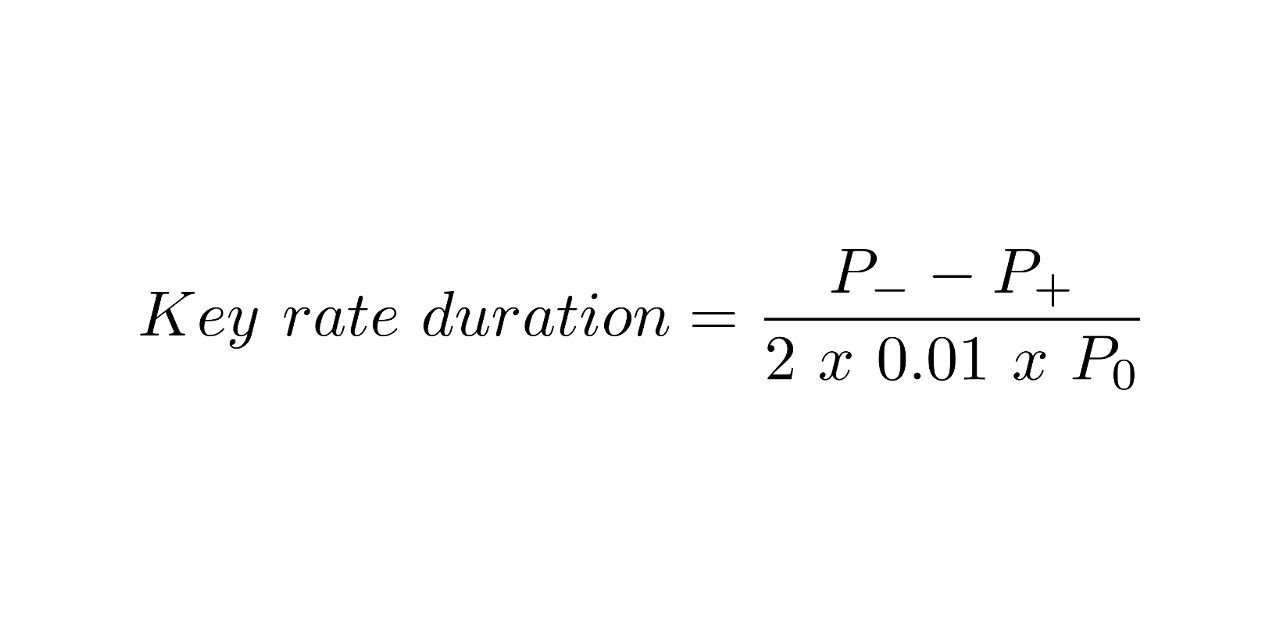

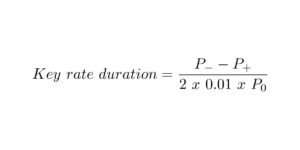

The Key Rate Duration Formula

File Photo: Key Rate Formula

P is the price of a security following a 1% drop in yield.

P+ is the security price following a 1% rise in yield.

P0 is the initial price of the security.

How to Compute Key Rate Duration

For illustration purposes, consider a bond initially valued at $1,000. It would be priced at $970 with a 1% increase in yield and $1,040 with a 1% fall in yield. The key rate duration for this bond would be, according to the preceding formula:

KRD = ($^1}, 0~4 0 →$ 9~7 0 ) / ( 2 ̗ 1 % Ï $ 1~, 0 0 0 ) = $ 7 0 / $ 2 0 = 3. 5 where:

Key rate duration, or KRD

KRD = (1,040 – $9700)/(2×1%×$1,000) = 70/$20 = 3.5

Key rate duration, or KRD

What Can You Learn From Key Rate Duration?

Since the yield curve frequently varies in a way that is not precisely parallel, critical rate duration is crucial in evaluating the projected changes in value for a bond or portfolio of bonds.

Another crucial bond metric is effective duration, a wise duration measure that estimates price changes for a bond or bond portfolio given a 1% change in yield. However, it is only applicable to parallel shifts in the yield curve. For this reason, the critical rate duration is a handy metric.

Effective duration and critical rate duration are connected. The Treasury spot rate curve has 11 maturities; a critical rate duration can be computed for each. The portfolio’s effective duration equals the sum of the 11 significant rate durations along the yield curve.

An Illustration of the Use of the Key Rate Duration

Because it is doubtful that one point on the Treasury yield curve will shift upward or downward while all other points stay constant, it can be challenging to interpret a single critical rate duration. It helps examine critical rate durations across the curve and comparethe relative fundamental rate duration values of two decurities.

For illustration purposes, assume that bond X has a crucial rate duration of 0.5 for one year and 0.9 for five years. Bond Y’s critical rate durations for these maturity points are 1.2 and 0.3, respectively. Bond X is half as sensitive to interest rate changes as bond Y on the short-term end of the curve, and bond Y is one-third as sensitive on the intermediate part of the curve.

Conclusion

- It figures out how much the price of a bond changes when the yield for a specific term changes by 100 basis points, or 1%.

- If the yield curve moves parallelly, you can use effective duration to determine how much the portfolio’s value has changed. But if the yield curve moves non-parallelly, you must use critical rate duration.

- If interest rates change, duration measures let you know how much of a price risk it is to hold fixed-income assets.