What is the hierarchy of GAAP?

The hierarchy of GAAP is a four-level framework ranking FASB, SEC, and AICPA guidance on accounting practices and standards by authority. Top-level guidance covers general accounting concerns, whereas lower-level guidance covers technical issues.

Understanding GAAP Hierarchy

With several regulatory agencies monitoring different aspects of accounting, it was necessary to identify the most relevant and authoritative recommendations. Each regulatory agency publishes accounting guidelines in numerous ways with different authorities. The GAAP hierarchy improves financial reporting uniformity and comparability. This framework helps accountants choose principles for preparing non-governmental financial statements under U.S. GAAP.

Financial Accounting Standards Board

A 1973-founded independent nonprofit, the FASB sets accounting and financial reporting rules for U.S. public and private enterprises and nonprofits. This standardizes reporting, helping investors and other financial statement consumers compare financial statements from firms in a sector or industry.

Securities and Exchange Commission

Established in 1934, the SEC is an independent federal body that safeguards investors, ensures fair and orderly securities markets, and promotes capital formation. The SEC regulates public company reporting.

The AICPA

Since 1887, the AICPA has been the nonprofit professional association representing CPAs in the U.S. AICPA requirements for private company external audits are among its duties.

GAAP Hierarchy Requirements

The GAAP hierarchy has four levels. Top-level instruction is more authoritative. An accountant exploring a topic should seek top-level guidance. The accountant should seek the next level for pertinent announcements if the upper levels don’t provide information.

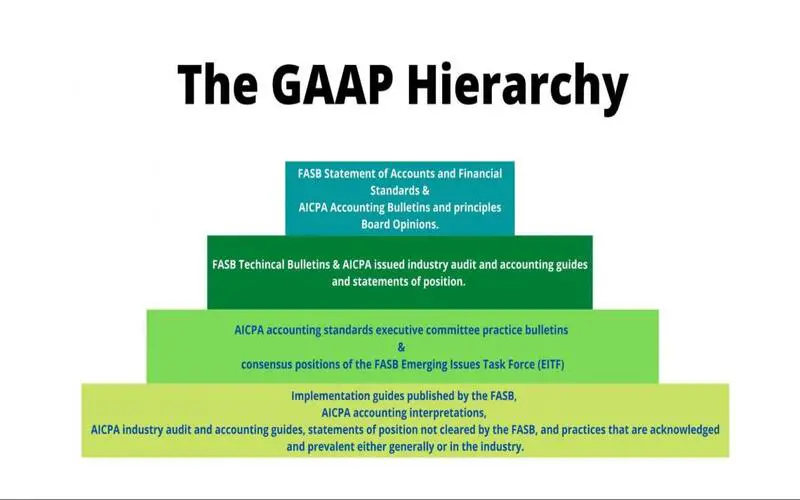

FASB statements and interpretations, SEC rules and interpretative releases (for all SEC registrants), and AICPA accounting research bulletins and views top the GAAP hierarchy.

The second level includes FASB Technical Bulletins and, if cleared, AICPA Industry Audit and Accounting Guides and Statements of Position.

The third level includes AICPA Accounting Standards Executive Committee Practice Bulletins, FASB Emerging Issues Task Force (EITF) consensus views, and Appendix D of EITF Abstracts subjects.

FASB implementation guidelines, AICPA accounting interpretations, and unapproved AICPA industry audit and accounting guidelines and position statements are the lowest level. The lowest level includes generally known and applied accounting techniques in general or in a specific industry.

The FASB’s Statement of Accounting Standards No. 162 explains the hierarchy.

Conclusion

- The four-tiered GAAP hierarchy helps accountants choose principles for nongovernmental entity financial reporting.

- Identifying the most applicable standards for diverse accounting issues was necessary since several organizations control different accounting areas.

- The hierarchy of GAAP determines which rules and best practices apply to a particular issue.

- The accountant should check the next level for relevant statements if the upper levels don’t provide information.