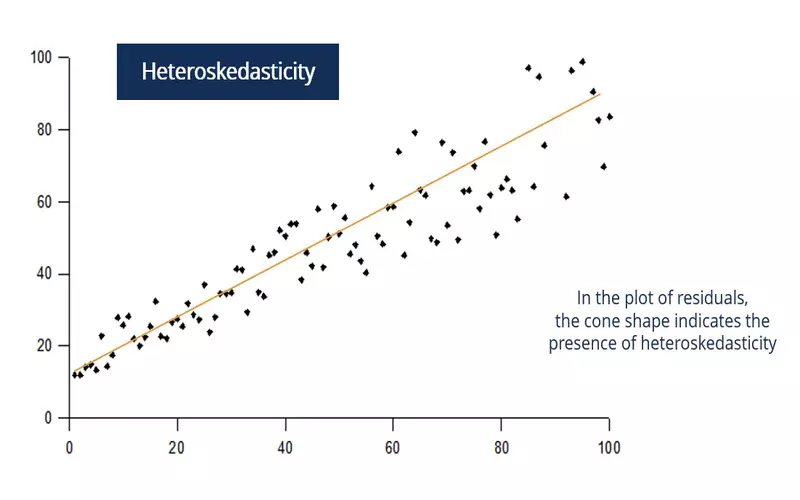

Definition of Heteroskedastic

Heteroskedasticity occurs when the residual term, or error term, in a regression model has significant variation. If so, it may fluctuate systematically and have an explanation. Changing the model to explain systematic variance using one or more predictor variables may improve its definition. The opposite of heteroskedasticity is homoskedasticity. Homoskedasticity is when the residual term variance is constant or close to it. Linear regression assumes homoskedasticity (or “heteroskedastic”). The regression model may be well-defined if homoskedasticity explains the dependent variable’s performance.

BREAKDOWN

Using heteroskedasticity in regression modeling is crucial for understanding the financial business’s performance of securities and investment portfolios. The highly popular Capital Asset Pricing Model (CAPM) analyzes stock performance based on its volatility compared to the market. Expanded versions of this concept include size, momentum, quality, and style (value vs. growth).

These predictor factors explain portfolio performance variation, which CAPM explains. The CAPM model’s architects knew their model couldn’t explain an exciting anomaly: high-quality equities, less volatile than low-quality stocks, performed better than projected. CAPM suggests higher-risk stocks beat lower-risk ones. In other words, high-volatility equities should defeat low-volatility ones. However, less volatile, high-quality companies outperformed CAPM.

Later, other researchers added quality as a “factor” to the CAPM model, which included size, style, and momentum. Adding this element to the model explained low-volatility stock performance anomalies. Multi-factor models underpin factor investing and smart beta.