The Heath-Jarrow-Morton (HJM) Model?

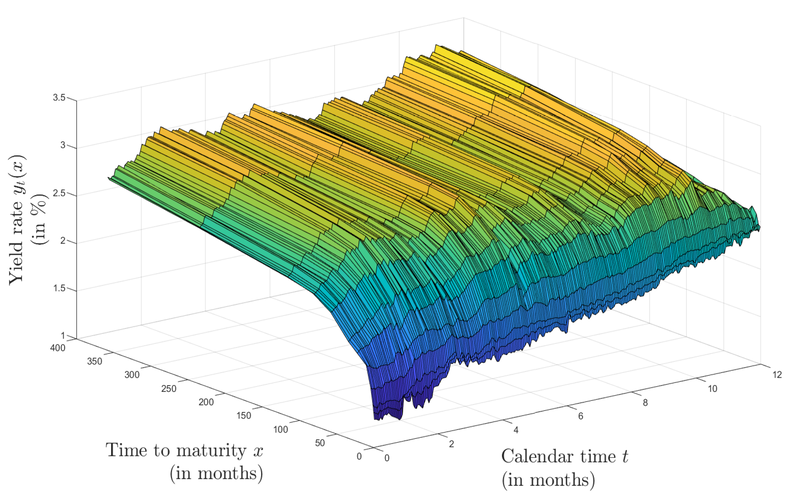

The Heath-Jarrow-Morton Model (HJM) helps predict future interest rates. Modeling these rates with an existing interest rate structure determines suitable pricing for interest-sensitive securities.

Formula for HJM Model

HJM models and others based on it follow the formula:

df(t,T)=α(t,T)dt+σ(t,T)dW(t)

Where:

The df(t, T) equation assumes that a zero-coupon bond’s instantaneous future interest rate with maturity T follows the stochastic differential equation.

α,σ=Adapted

The Brownian motion (random walk) under the risk-neutral assumption is W.

The HJM Model: What Does It Say?

The Heath-Jarrow-Morton Model is a highly theoretical tool for advanced financial analysis. Many arbitrageurs and analysts utilize it to find arbitrage opportunities and price derivatives. The sum of drift and diffusion factors starts the HJM Model’s forward interest rate prediction. The HJM drift condition, or volatility, drives forward rate drift. A HJM model is any interest rate model with a finite number of Brownian movements.

The 1980s work of economists David Heath, Robert Jarrow, and Andrew Morton inspired the HJM Model. In the late 1980s and early 1990s, the trio published papers such as “Bond Pricing and the Term Structure of Interest Rates: A Discrete Time Approximation,” “Contingent Claims Valuation with a Random Evolution of Interest Rates,” and “Bond Pricing and the Term Structure of Interest Rates: A New Methodology for Contingent Claims Valuation” that established the framework.

Several HJM framework models exist. They all try to estimate the complete forward rate curve, not simply the short rate or another point. The major problem with HJM models is their unlimited dimensions, making computation nearly impossible. Several models attempt to express the HJM model finitely.

Option Pricing with HJM Model

Option pricing uses the HJM Model to determine the fair value of derivative contracts. Trading institutions may price options using models to locate undervalued or overpriced options.

Mathematical pricing models calculate option values using known inputs and projected variables, like implied volatility. Traders calculate pricing using models and update them based on risk.

To determine the value of an interest rate swap in an HJM model, create a discount curve using current option prices. We can calculate forward rates from that discount curve. From there, input forwarding interest rate volatility is used to calculate drift.

Conclusion

- Heath-Jarrow-Morton (HJM) models forward interest rates using a random differential equation.

- Modeling these rates with an existing term structure of interest rates determines bond and exchange pricing.

- Arbitrageurs and derivatives analysts mainly utilize it today.