The Average True Range (ATR): What Is It?

Market specialist J. Welles Wilder Jr. established the average true range (ATR). In his book New Concepts in Technical Trading Systems, this technical analysis indicator analyzes market volatility by breaking down the whole range of an asset price for that period.

The current high minus the current low, the current high’s absolute value minus the previous close, and the current low’s absolute value minus the previous close are the three most significant values representing the accurate range indication. The ATR is a moving average of the actual ranges, often calculated over 14 days.

While longer intervals have a higher possibility of producing fewer trading signals, traders can employ shorter periods than 14 days to create more trading signals.

It would be best if you first used the following formula to calculate the valid range:

H=Today’s high

L=Today’s low

Cp= Yesterday’s closing price

Max=Highest value of the three terms

(H−L)=Today’s high minus the low∣

H−Cp∣=Absolute value of today’s high minus Yesterday’s closing price∣

L−Cp∣=Absolute value of today’s low minus Yesterday’s closing price

How to Calculate the ATR

The first step in calculating ATR is to find a series of actual range values for a security. The price range of an asset for a given trading day is its high minus its low. To find an asset’s actual range value, determine the formula’s three terms.

Suppose that XYZ’s stock had a trading high today of $21.95 and a low of $20.22. It closed yesterday at $21.51. Using the three terms, we get the highest result:

∣(H−C)∣=∣$21.95−$21.51∣=$0.44

∣(L−C)∣=∣$20.22−$21.51∣=$1.29

Because you don’t have a previous ATR, you need to use the ATR formula:

(n1)i∑nTRi

Using 14 days as the number of periods, you’d calculate the TR for each of the 14 days. Assume the following prices from the table.

| Daily Values | |||

|---|---|---|---|

| High | Low | Yesterday’s Close | |

| Day 1 | $ 21.95 | $ 20.22 | $ 21.51 |

| Day 2 | $ 22.25 | $ 21.10 | $ 21.61 |

| Day 3 | $ 21.50 | $ 20.34 | $ 20.83 |

| Day 4 | $ 23.25 | $ 22.13 | $ 22.65 |

| Day 5 | $ 23.03 | $ 21.87 | $ 22.41 |

| Day 6 | $ 23.34 | $ 22.18 | $ 22.67 |

| Day 7 | $ 23.66 | $ 22.57 | $ 23.05 |

| Day 8 | $ 23.97 | $ 22.80 | $ 23.31 |

| Day 9 | $ 24.29 | $ 23.15 | $ 23.68 |

| Day 10 | $ 24.60 | $ 23.45 | $ 23.97 |

| Day 11 | $ 24.92 | $ 23.76 | $ 24.31 |

| Day 12 | $ 25.23 | $ 24.09 | $ 24.60 |

| Day 13 | $ 25.55 | $ 24.39 | $ 24.89 |

| Day 14 | $ 25.86 | $ 24.69 | $ 25.20 |

You’d use these prices to calculate the TR for each day.

| Trading Range | |||

|---|---|---|---|

| H-L | H-Cp | L-Cp | |

| Day 1 | $ 1.73 | $ 0.44 | $ (1.29) |

| Day 2 | $ 1.15 | $ 0.64 | $ (0.51) |

| Day 3 | $ 1.16 | $ 0.67 | $ (0.49) |

| Day 4 | $ 1.12 | $ 0.60 | $ (0.52) |

| Day 5 | $ 1.15 | $ 0.61 | $ (0.54) |

| Day 6 | $ 1.16 | $ 0.67 | $ (0.49) |

| Day 7 | $ 1.09 | $ 0.61 | $ (0.48) |

| Day 8 | $ 1.17 | $ 0.66 | $ (0.51) |

| Day 9 | $ 1.14 | $ 0.61 | $ (0.53) |

| Day 10 | $ 1.15 | $ 0.63 | $ (0.52) |

| Day 11 | $ 1.16 | $ 0.61 | $ (0.55) |

| Day 12 | $ 1.14 | $ 0.63 | $ (0.51) |

| Day 13 | $ 1.16 | $ 0.66 | $ (0.50) |

| Day 14 | $ 1.17 | $ 0.66 | $ (0.51) |

You find that the highest values for each day are from the (H – L) column, so you’d add up all of the results from the (H – L) column and multiply the result by 1/n, per the formula.

1�($16.65)=114($16.65)

0.714×$16.65=$1.18

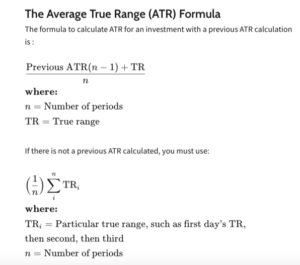

So, the average volatility for this asset is $1.18. Now that you have the ATR for the previous period, you can use it to determine the ATR for the current period using the following:

Previous ATR(−1)+TR

This formula is much simpler because you only need to calculate the TR for one day. Assuming on Day 15, the asset has a high of $25.55, a low of $24.37, and closed the previous day at $24.87, its TR works out to $1.18:

$1.18(14−1)+$1.1814

$1.18(13)+$1.1814

$15.34+$1.1814

$16.5214=$1.18

The stock closed the day again with an average volatility (ATR) of $1.18.

What Can You Learn From the ATR?

Although stocks and indices may also be employed with the indicator, Wilder initially created the ATR for commodities.

In other words, a greater ATR corresponds to increased volatility in the stock during the time under review, while a smaller ATR denotes reduced volatility. Market technicians can use the ATR as a helpful tool to add to a trading strategy and to enter and exit deals. It was developed to enable traders to use basic mathematics to determine an asset’s daily volatility with greater accuracy. The indicator’s primary function is to quantify gap-induced volatility and limit upward or downward movement; it does not display price direction. Calculating the ATR is relatively easy and requires simply past price data.

The ATR is frequently employed as an exit strategy regardless of the entering decision-making process. Chuck LeBeau is credited with creating one well-liked method called the “chandelier exit.” “The chandelier exit sets up a trailing stop below the stock’s highest closing price since you joined the transaction. The distance between the highest high and the stop level is defined by multiple times the ATR.

IAtrader may also utilize the ATR to determine the appropriate transaction size in the derivatives markets. The ATR technique may be used to determine a position size that considers both the volatility of the underlying market and the willingness of each trader to take on risk.

An Illustration of Using the ATR

For example, let’s say the sixth day’s actual range is 1.09, and the first value of a five-day ATR is 1.41. One way to estimate the sequential ATR value is to multiply the previous Ay by the number of days minus one and add the actual range for the current period to the result.

After that, divide the sum by the chosen time frame. For instance, 1.35, or (1.41 * (5 – 1) + (1.09)) / 5, is expected to represent the second value of the ATR. The whole duration might then be covered by repeating the calculation.

Although the ATR can not predict the breakout’s direction, it may be added to the closing price, and if the price moves above that figure the next day, the trader can purchase. The concept is displayed below. While trading signals are not standard, they often hint at essential breakthroughs. These indications are based on the theory that volatility changes when the price closes more than an average true range above the previous close.

The ATR’s limitations

Using the ATR indicator has two key drawbacks. First, ATR is a subjective metric that may be interpreted in various ways. It is impossible to predict with 100% accuracy if a trend will turn around based on an ATR number. To determine a trend’s strength or weakness, ATR measurements should instead always be compared to previous readings.

Secondly, ATR does not account for price direction; it just gauges volatility. This can occasionally produce contradictory signals, mainly when pivots occur in the markets or trends are approaching turning points. An abrupt spike in the ATR after a significant move against the current trend, for example, might mislead specific traders into believing that the ATR is reaffirming the previous trend.

In trading, how is the ATR indicator used?

The price volatility of an investment is assessed using the average true range. It is used to initiate and exit trades and make asset purchases with other indicators and tools.

How are ATR values read?

An investment’s average price range over time is known as its average actual range value. For an asset, this means that an average trading day’s range of fluctuation in price is $1.18 if the asset’s ATR is $1.18.

Which average true range is the best?

ATR quality is asset-specific. Its performance can be considered typical if its average trading volume (ATR) is consistently near $1.18. It may be necessary to conduct more research if the same asset suddenly has an ATR greater than $1.18. Similarly, you should investigate the reason(s) before acting if the ATR is significantly lower.

The average true range of an asset can help determine its price volatility. Rather than serving as a trend indicator, its ideal application is to ascertain how much the price of an investment has moved over the period under review. The only thing you need to utilize to calculate an investment’s ATR is price data for the period you are researching.

Conclusion

- Technical analysis uses the average true range (ATR) as a market volatility indicator.

- Usually, a 14-day simple moving average of many genuine range indicators is used to calculate it.

- Although the ATR was first created for the commodities markets, it is now used for many securities.

- The average range price swing for an investment over a certain period is displayed to investors via the ATR.