What is sampling?

In statistical analysis, sampling is the procedure by which researchers choose a predefined number of observations from a larger population. Sampling enables researchers to use a tiny percentage of the population to study a large group. The sampling strategy may include systematic or essential random sampling, depending on the study type. In the fields of statistics, psychology, and finance, sampling is often used.

How Sampling Works

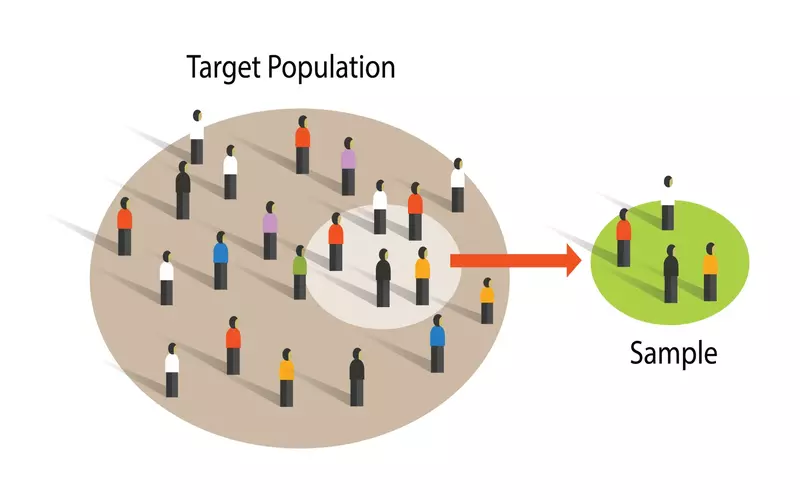

Accurate studies on huge populations might be challenging for scientists. It may only sometimes be feasible to examine some members of the group. They often choose a tiny section to symbolize the whole group because of this. We refer to this as a sample. With samples, researchers may estimate the size of the broader population by using the features of the small group.

A representative sample of the whole population should have been selected. When drawing from a broader population, choosing a sample is essential. A representative sample has to be picked randomly and include every member of the population. For instance, by selecting 10% of the student population, a lottery method may be used to ascertain the average age of students at an institution.

Sampling is often used in economic research involving sizable segments of the population. For example, the U.S. Bureau of Labor Statistics (BLS) uses sampling in its monthly employment report, which reports:

One hundred twenty-two thousand companies and government organizations were used to compile the Current Employment Statistics.

The Current Population Survey used a nationwide sample of 60,000 distinct homes.

Researchers should recognize errors in sampling. This happens when the chosen sample is representative of only some of the population. This indicates that the sample’s findings differ from the population’s. Sampling mistakes may be the result of bias or happen at random. For example, some sample group members could decide not to take part, or they might be different from other participants in some manner.

Since sampling isn’t a precise science, conclusions should be interpreted broadly. Extrapolating from the sample group, generalizations about the larger population are not advised.

Audit Sampling Types

As was already said, researchers might use a variety of sampling techniques. They consist of judgment, random, block, and systemic sampling. We go into more depth about them below.

Haphazard sampling

Every item in a population has an equal chance of being selected when sampling is done at random. Due to the need for more human judgment in the sample selection process, it is the least susceptible to bias.

In a firm with 250 workers, selecting the names of 25 employees at random from a hat is an example of a random sample. There are 250 workers in the population, and because everyone has an equal chance of being selected, the sample is random.

Selection of Judgments

The sample may be chosen randomly from the whole population using auditor discretion. Only transactions of a significant nature may worry an auditor. Assume, for instance, that the auditor establishes a $10,000 threshold for accounts payable transaction materiality. Due to the limited population, the auditor may decide to investigate every transaction if the client provides a comprehensive record of all 15 transactions totaling more than $10,000.

Another option for the auditor is to include any general ledger account that differs by more than 10% from the previous quarter. In this instance, the population from which the sample selection is drawn is being restricted by the auditor. Unfortunately, explicit or implicit bias is always possible when human judgment is involved in sampling.

Block Counting

A sequential set of items from the population is used as the sample in block sampling. For instance, many methods exist to arrange a list of all sales transactions made during an accounting period, such as by date or quantity.

To choose a sample from a particular section of the list, an auditor may ask the company’s accountant to supply the list in one format or another. The auditor will likely need to make relatively few changes to this system, although a block of transactions may not accurately reflect the population.

Methodical Sampling

Systematic sampling selects items for a sample using a defined periodic interval, beginning at a random starting point within the population—the sampling interval results from dividing the population by the sample size. If the periodic interval is predetermined and the beginning point is random, systematic sampling is still regarded as random, even if the sample population has been chosen in advance.

Let’s say an auditor checks internal controls for a firm’s cash account and wants to verify the company policy stating that two individuals must sign checks above $10,000. Every firm check that exceeded $10,000 throughout the fiscal year—300 in this case—belongs to the population. The auditor concludes that the sample size using probability statistics should be 20% of the population or 60 checks. There is a 5 or 300 checks ÷ 60 sample checks sampling period.

As a result, the auditor chooses to examine every fifth check. The statistical analysis provides the auditor with a 95% confidence rate that the check technique was carried out properly, assuming that no mistakes are discovered in the sample test work. The auditor determines that the internal control over cash is operating effectively after testing the sample of 60 checks and finding no mistakes.

Market Sampling Example: Sampling companies want to reach specific markets with their goods and services. Businesses often ascertain the requirements and preferences of their target market before introducing items to the market. To achieve this, they could use sampling of the target market demographic to understand those requirements better and then develop a product or service that addresses those needs. In this instance, obtaining the sample’s perspective aids in determining the demands of the whole.

Samples of Audits

A certified public accountant (CPA) may utilize sampling in a financial audit to assess the completeness and integrity of account balances in their client’s financial statements. We refer to this as audit sampling.

Audit sampling is required when the population (the account transaction data) is significant.

Sampling error: What is it?

When the sample selected for analysis doesn’t represent the whole population under investigation, it results in a sampling error. This puts the validity and accuracy of the research at risk. For example, sampling error happens when researchers attempt to find out how students feel about their university experience by including professors in the sample. Random mistakes in sampling may also originate from bias of some kind.

Cluster Sampling: What Is It?

One kind of probability sampling is cluster sampling. Researchers split the population into smaller groups to do cluster sampling. Then, they randomly choose people from these categories to create their samples and conduct their research. This sampling is used when the sample size and population are too large to manage.

What Separates Non-Probability Sampling from Probability Sampling?

Using probability sampling, researchers may draw more robust conclusions about the population under study. Every member of the group has an equal chance of being selected as a representative sample of the whole population since random sampling is used in this process. The outcome is often objective.

On the other hand, non-probability sampling makes it simple for researchers to get data. This sampling is often biased as it’s impossible to predict which people will be included in the sample.

The Final Word

For research purposes, statisticians often use sampling when working with significant populations. Selecting a small sample of individuals from a larger group is known as sampling. This is often discovered when population data collection is required for statistical analysis, demographic surveys, and economic research.

Conclusion

- By using a small group from a broader population, sampling enables researchers to draw observations and conclusions.

- There are many different types of sampling, such as systematic, block, judgment, and random sampling.

- Sampling mistakes concern researchers because they might arise from bias or random sampling.

- Sampling is a marketing strategy used by companies to determine the requirements and preferences of their target market.

- During audits, sampling is a tool used by certified public accountants to assess the completeness and correctness of account balances.